Even With A 32% Surge, Cautious Investors Are Not Rewarding WindowMaster International A/S' (CPH:WMA) Performance Completely

WindowMaster International A/S (CPH:WMA) shares have continued their recent momentum with a 32% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 35% in the last year.

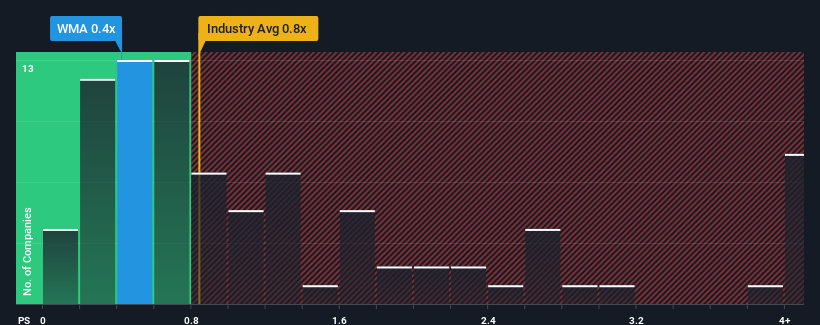

Even after such a large jump in price, there still wouldn't be many who think WindowMaster International's price-to-sales (or "P/S") ratio of 0.4x is worth a mention when the median P/S in Denmark's Building industry is similar at about 0.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for WindowMaster International

What Does WindowMaster International's Recent Performance Look Like?

As an illustration, revenue has deteriorated at WindowMaster International over the last year, which is not ideal at all. It might be that many expect the company to put the disappointing revenue performance behind them over the coming period, which has kept the P/S from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on WindowMaster International will help you shine a light on its historical performance.What Are Revenue Growth Metrics Telling Us About The P/S?

WindowMaster International's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 1.4%. Regardless, revenue has managed to lift by a handy 26% in aggregate from three years ago, thanks to the earlier period of growth. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 2.5% shows it's noticeably more attractive.

With this information, we find it interesting that WindowMaster International is trading at a fairly similar P/S compared to the industry. It may be that most investors are not convinced the company can maintain its recent growth rates.

What Does WindowMaster International's P/S Mean For Investors?

WindowMaster International appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We didn't quite envision WindowMaster International's P/S sitting in line with the wider industry, considering the revenue growth over the last three-year is higher than the current industry outlook. When we see strong revenue with faster-than-industry growth, we can only assume potential risks are what might be placing pressure on the P/S ratio. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

Having said that, be aware WindowMaster International is showing 3 warning signs in our investment analysis, and 2 of those shouldn't be ignored.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if WindowMaster International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About CPSE:WMA

WindowMaster International

Engages in the development, production, marketing, and sale of natural and mixed mode ventilation, smoke and heat ventilation, and automatic window control solutions for the commercial construction industry worldwide.

Excellent balance sheet and good value.

Market Insights

Community Narratives