Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like NKT (CPH:NKT). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide NKT with the means to add long-term value to shareholders.

See our latest analysis for NKT

How Fast Is NKT Growing Its Earnings Per Share?

In the last three years NKT's earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. As a result, we'll zoom in on growth over the last year, instead. In impressive fashion, NKT's EPS grew from €0.59 to €1.66, over the previous 12 months. It's a rarity to see 179% year-on-year growth like that.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. The music to the ears of NKT shareholders is that EBIT margins have grown from 1.6% to 5.7% in the last 12 months and revenues are on an upwards trend as well. Both of which are great metrics to check off for potential growth.

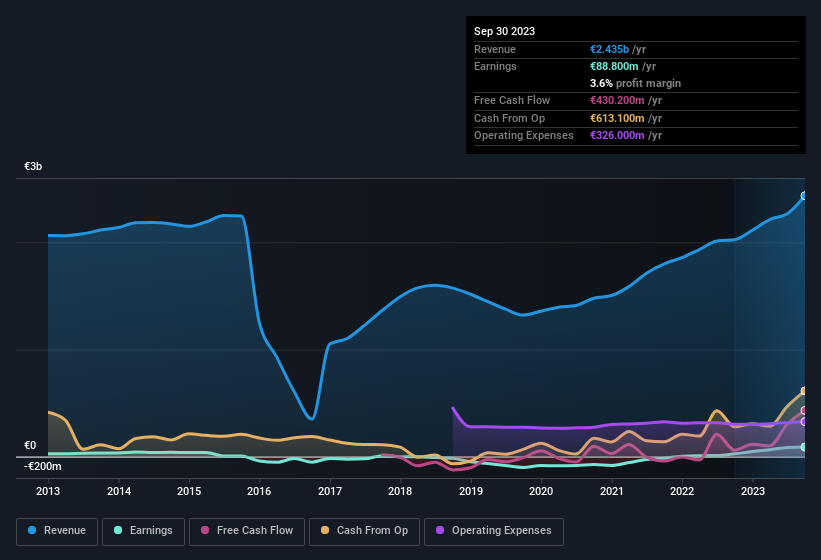

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for NKT's future profits.

Are NKT Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

For the sake of balance, it should be noted that NKT insiders sold €696k worth of shares last year. This falls short of the share acquisition by Chairman of the Board Jens Peter Olsen, who has acquired €1.2m worth of shares, at an average price of €395. Overall, that is something good to take away.

Is NKT Worth Keeping An Eye On?

NKT's earnings per share growth have been climbing higher at an appreciable rate. Growth investors should find it difficult to look past that strong EPS move. And indeed, it could be a sign that the business is at an inflection point. If this these factors intrigue you, then an addition of NKT to your watchlist won't go amiss. Don't forget that there may still be risks. For instance, we've identified 1 warning sign for NKT that you should be aware of.

Keen growth investors love to see insider buying. Thankfully, NKT isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if NKT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CPSE:NKT

NKT

Develops, manufactures, and markets cables, accessories, and solutions in Denmark and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Community Narratives