Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Hapag-Lloyd Aktiengesellschaft (ETR:HLAG) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Hapag-Lloyd

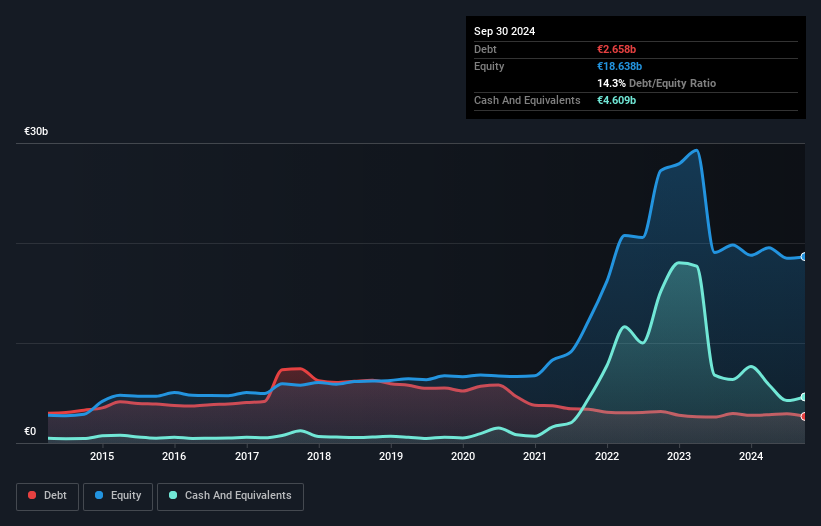

What Is Hapag-Lloyd's Net Debt?

As you can see below, Hapag-Lloyd had €2.66b of debt at September 2024, down from €2.94b a year prior. However, its balance sheet shows it holds €4.61b in cash, so it actually has €1.95b net cash.

How Strong Is Hapag-Lloyd's Balance Sheet?

According to the last reported balance sheet, Hapag-Lloyd had liabilities of €6.52b due within 12 months, and liabilities of €4.96b due beyond 12 months. On the other hand, it had cash of €4.61b and €2.57b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by €4.31b.

Since publicly traded Hapag-Lloyd shares are worth a very impressive total of €26.3b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Hapag-Lloyd boasts net cash, so it's fair to say it does not have a heavy debt load!

In fact Hapag-Lloyd's saving grace is its low debt levels, because its EBIT has tanked 74% in the last twelve months. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Hapag-Lloyd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Hapag-Lloyd has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Hapag-Lloyd actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

Although Hapag-Lloyd's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of €1.95b. And it impressed us with free cash flow of €1.4b, being 104% of its EBIT. So we don't have any problem with Hapag-Lloyd's use of debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with Hapag-Lloyd (including 2 which make us uncomfortable) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Hapag-Lloyd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:HLAG

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

17 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k12.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8688.6% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative