UniDevice AG's (ETR:UDC) Analyst Just Slashed This Year's Estimates

Today is shaping up negative for UniDevice AG (ETR:UDC) shareholders, with the covering analyst delivering a substantial negative revision to this year's forecasts. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analyst seeing grey clouds on the horizon.

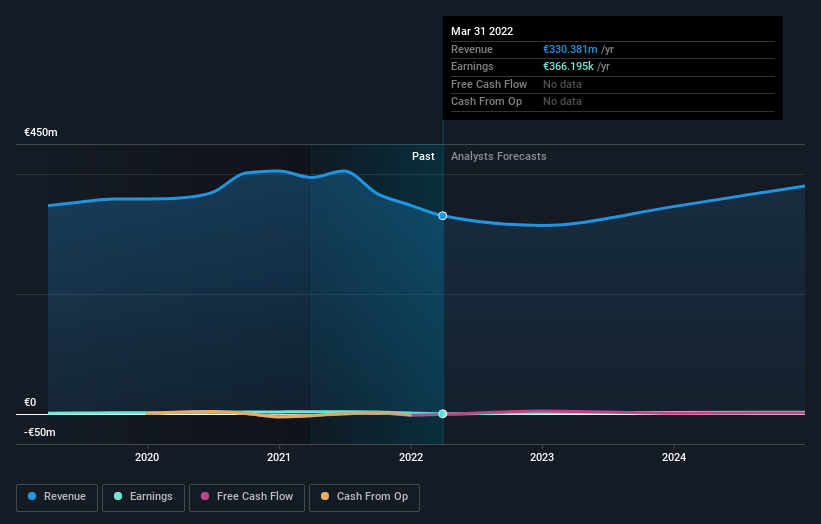

Following the downgrade, the consensus from sole analyst covering UniDevice is for revenues of €314m in 2022, implying a small 4.9% decline in sales compared to the last 12 months. Statutory earnings per share are presumed to bounce 475% to €0.14. Prior to this update, the analyst had been forecasting revenues of €369m and earnings per share (EPS) of €0.24 in 2022. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a pretty serious decline to earnings per share numbers as well.

See our latest analysis for UniDevice

The consensus price target fell 28% to €2.80, with the weaker earnings outlook clearly leading analyst valuation estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the UniDevice's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 4.9% by the end of 2022. This indicates a significant reduction from annual growth of 0.9% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 12% per year. It's pretty clear that UniDevice's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. After such a stark change in sentiment from the analyst, we'd understand if readers now felt a bit wary of UniDevice.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with UniDevice, including the risk of cutting its dividend. Learn more, and discover the 3 other flags we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:UDC

UniDevice

Together with its subsidiary PPA International AG, engages in wholesale of electronic entertainment and communication devices.

Undervalued with solid track record.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion