Is USU Software AG's (ETR:OSP2) Stock's Recent Performance Being Led By Its Attractive Financial Prospects?

Most readers would already be aware that USU Software's (ETR:OSP2) stock increased significantly by 11% over the past three months. Since the market usually pay for a company’s long-term fundamentals, we decided to study the company’s key performance indicators to see if they could be influencing the market. Particularly, we will be paying attention to USU Software's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for USU Software

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for USU Software is:

13% = €7.6m ÷ €57m (Based on the trailing twelve months to December 2022).

The 'return' is the income the business earned over the last year. Another way to think of that is that for every €1 worth of equity, the company was able to earn €0.13 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

USU Software's Earnings Growth And 13% ROE

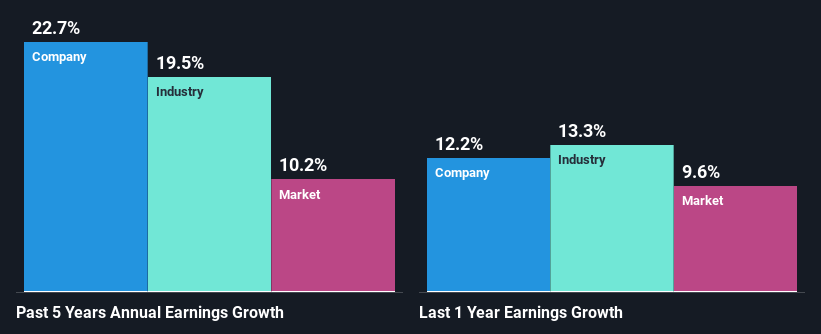

To begin with, USU Software seems to have a respectable ROE. And on comparing with the industry, we found that the the average industry ROE is similar at 15%. Consequently, this likely laid the ground for the impressive net income growth of 23% seen over the past five years by USU Software. However, there could also be other drivers behind this growth. Such as - high earnings retention or an efficient management in place.

As a next step, we compared USU Software's net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 20% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if USU Software is trading on a high P/E or a low P/E, relative to its industry.

Is USU Software Efficiently Re-investing Its Profits?

USU Software's significant three-year median payout ratio of 74% (where it is retaining only 26% of its income) suggests that the company has been able to achieve a high growth in earnings despite returning most of its income to shareholders.

Additionally, USU Software has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 44% over the next three years. However, the company's ROE is not expected to change by much despite the lower expected payout ratio.

Conclusion

In total, we are pretty happy with USU Software's performance. We are particularly impressed by the considerable earnings growth posted by the company, which was likely backed by its high ROE. While the company is paying out most of its earnings as dividends, it has been able to grow its earnings in spite of it, so that's probably a good sign. We also studied the latest analyst forecasts and found that the company's earnings growth is expected be similar to its current growth rate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:OSP2

USU Software

Provides software and service solutions for information technology (IT) and customer service management in Germany and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives