- Germany

- /

- Semiconductors

- /

- DB:GY9

Smoltek Nanotech Holding (FRA:GY9) Has Debt But No Earnings; Should You Worry?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Smoltek Nanotech Holding AB (FRA:GY9) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Smoltek Nanotech Holding's Net Debt?

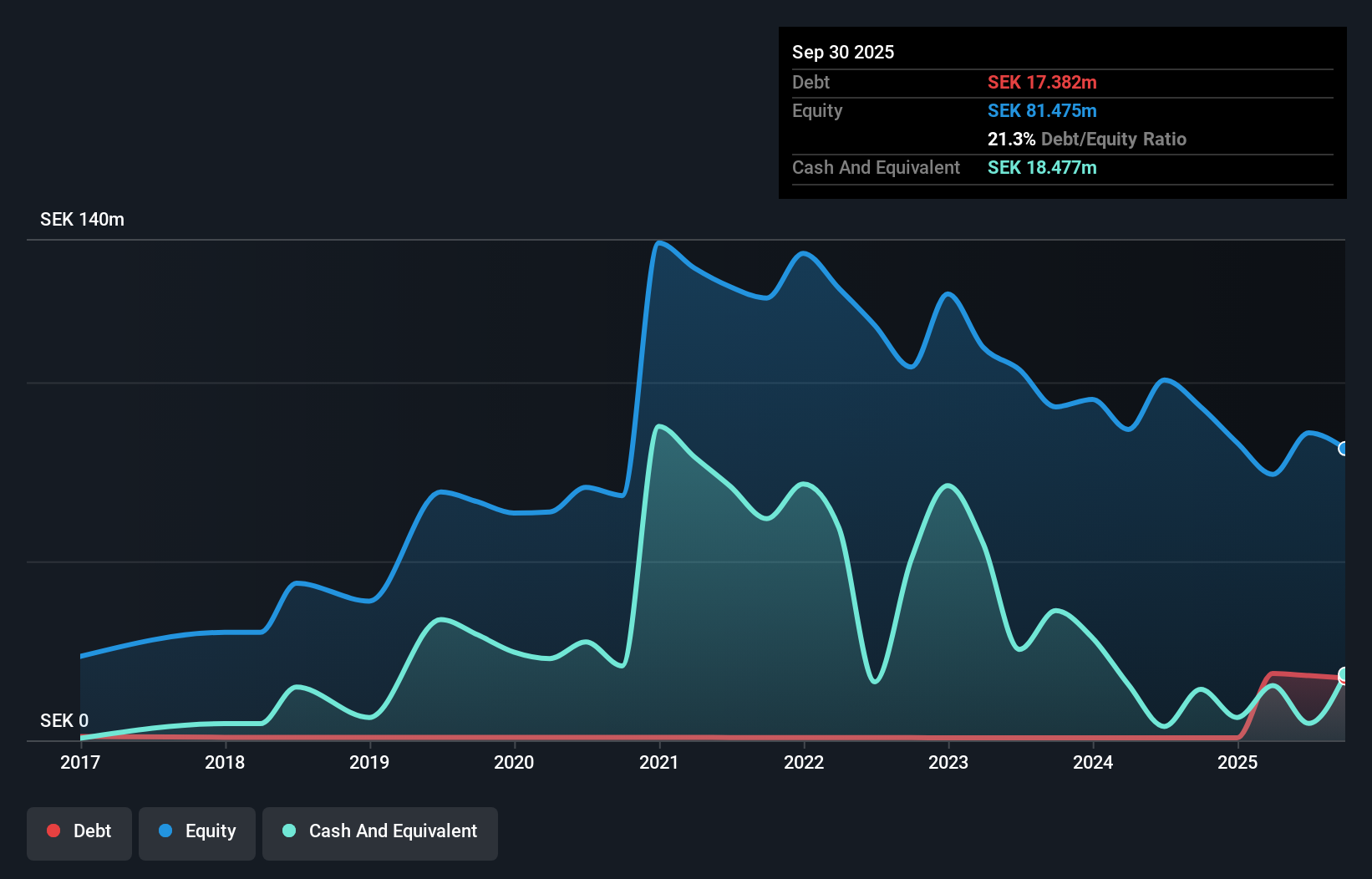

As you can see below, at the end of September 2025, Smoltek Nanotech Holding had kr17.4m of debt, up from kr682.0k a year ago. Click the image for more detail. However, it does have kr18.5m in cash offsetting this, leading to net cash of kr1.10m.

How Strong Is Smoltek Nanotech Holding's Balance Sheet?

We can see from the most recent balance sheet that Smoltek Nanotech Holding had liabilities of kr10.5m falling due within a year, and liabilities of kr17.4m due beyond that. Offsetting these obligations, it had cash of kr18.5m as well as receivables valued at kr7.10m due within 12 months. So it has liabilities totalling kr2.34m more than its cash and near-term receivables, combined.

Having regard to Smoltek Nanotech Holding's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the kr797.5m company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, Smoltek Nanotech Holding also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is Smoltek Nanotech Holding's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

View our latest analysis for Smoltek Nanotech Holding

In the last year Smoltek Nanotech Holding had a loss before interest and tax, and actually shrunk its revenue by 63%, to kr3.5m. That makes us nervous, to say the least.

So How Risky Is Smoltek Nanotech Holding?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Smoltek Nanotech Holding lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of kr38m and booked a kr38m accounting loss. With only kr1.10m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 6 warning signs for Smoltek Nanotech Holding (of which 5 are potentially serious!) you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DB:GY9

Smoltek Nanotech Holding

Develops nanostructure fabrication technology for the semiconductor industry in Sweden.

Medium-low risk with mediocre balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)