Advertisement

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Although, when we looked at Siltronic (ETR:WAF), it didn't seem to tick all of these boxes.

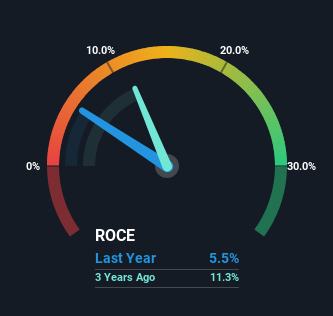

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Siltronic is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.055 = €213m ÷ (€4.5b - €638m) (Based on the trailing twelve months to December 2023).

Thus, Siltronic has an ROCE of 5.5%. Ultimately, that's a low return and it under-performs the Semiconductor industry average of 16%.

See our latest analysis for Siltronic

Above you can see how the current ROCE for Siltronic compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Siltronic .

What Does the ROCE Trend For Siltronic Tell Us?

On the surface, the trend of ROCE at Siltronic doesn't inspire confidence. Around five years ago the returns on capital were 31%, but since then they've fallen to 5.5%. And considering revenue has dropped while employing more capital, we'd be cautious. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

The Bottom Line

We're a bit apprehensive about Siltronic because despite more capital being deployed in the business, returns on that capital and sales have both fallen. Despite the concerning underlying trends, the stock has actually gained 8.1% over the last five years, so it might be that the investors are expecting the trends to reverse. Either way, we aren't huge fans of the current trends and so with that we think you might find better investments elsewhere.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for Siltronic (of which 2 are significant!) that you should know about.

While Siltronic may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:WAF

Siltronic

Develops, produces, markets, and sells hyperpure silicon wafers for the semiconductor industry in Germany, rest of Europe, the United States, Taiwan, Mainland China, South Korea, rest of Asia, and internationally.

Slight risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor