Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Sedlmayr Grund und Immobilien AG (FRA:SPB) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Sedlmayr Grund und Immobilien

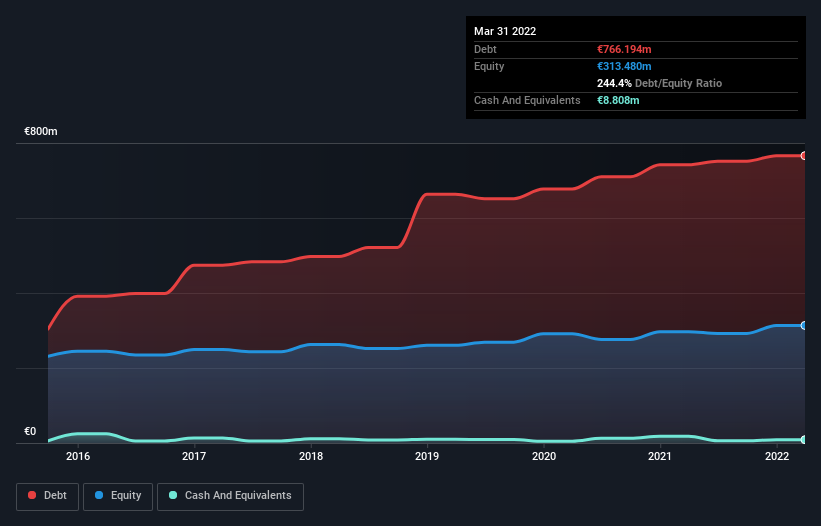

How Much Debt Does Sedlmayr Grund und Immobilien Carry?

The chart below, which you can click on for greater detail, shows that Sedlmayr Grund und Immobilien had €766.2m in debt in March 2022; about the same as the year before. And it doesn't have much cash, so its net debt is about the same.

How Strong Is Sedlmayr Grund und Immobilien's Balance Sheet?

The latest balance sheet data shows that Sedlmayr Grund und Immobilien had liabilities of €2.62m due within a year, and liabilities of €844.4m falling due after that. Offsetting these obligations, it had cash of €8.81m as well as receivables valued at €211.8m due within 12 months. So it has liabilities totalling €626.4m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Sedlmayr Grund und Immobilien is worth €2.17b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Sedlmayr Grund und Immobilien's debt to EBITDA ratio of 9.6 suggests a heavy debt load, its interest coverage of 7.9 implies it services that debt with ease. Overall we'd say it seems likely the company is carrying a fairly heavy swag of debt. One way Sedlmayr Grund und Immobilien could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 16%, as it did over the last year. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Sedlmayr Grund und Immobilien will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, Sedlmayr Grund und Immobilien recorded free cash flow of 33% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Sedlmayr Grund und Immobilien's net debt to EBITDA was a real negative on this analysis, although the other factors we considered were considerably better. There's no doubt that it has an adequate capacity to grow its EBIT. Looking at all this data makes us feel a little cautious about Sedlmayr Grund und Immobilien's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 1 warning sign for Sedlmayr Grund und Immobilien that you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DB:SPB

Sedlmayr Grund und Immobilien

Develops and manages real estate properties in Germany.

Proven track record second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor