- Singapore

- /

- Specialized REITs

- /

- SGX:DCRU

3 Stocks That May Be Undervalued By Up To 48.7%

Reviewed by Simply Wall St

As global markets show signs of recovery with U.S. indexes approaching record highs and positive sentiment driven by strong labor market data, investors are keenly observing potential opportunities in undervalued stocks. In such a climate, identifying stocks that may be trading below their intrinsic value can offer significant investment potential, especially when broader market gains suggest underlying economic resilience.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Victory Capital Holdings (NasdaqGS:VCTR) | US$72.24 | US$144.03 | 49.8% |

| NBT Bancorp (NasdaqGS:NBTB) | US$50.12 | US$99.93 | 49.8% |

| BP Plastics Holding Bhd (KLSE:BPPLAS) | MYR1.20 | MYR2.39 | 49.7% |

| Synovus Financial (NYSE:SNV) | US$57.97 | US$115.67 | 49.9% |

| Intermedical Care and Lab Hospital (SET:IMH) | THB4.94 | THB9.86 | 49.9% |

| EuroGroup Laminations (BIT:EGLA) | €2.728 | €5.42 | 49.7% |

| Nidaros Sparebank (OB:NISB) | NOK100.00 | NOK198.62 | 49.7% |

| Nutanix (NasdaqGS:NTNX) | US$72.35 | US$143.99 | 49.8% |

| SBI Sumishin Net Bank (TSE:7163) | ¥2914.00 | ¥5793.07 | 49.7% |

| VerticalScope Holdings (TSX:FORA) | CA$9.01 | CA$18.01 | 50% |

Underneath we present a selection of stocks filtered out by our screen.

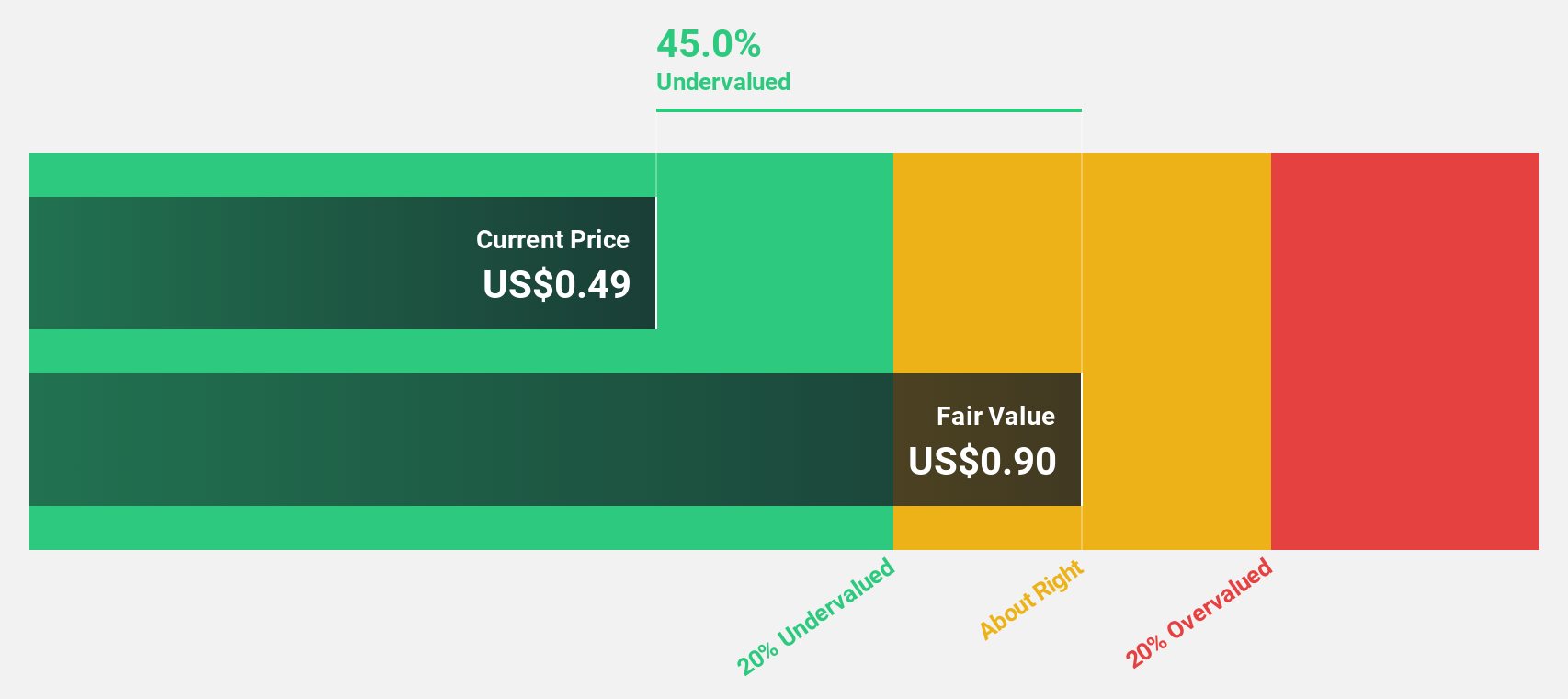

Digital Core REIT (SGX:DCRU)

Overview: Digital Core REIT (SGX: DCRU) is a Singapore-listed pure-play data centre real estate investment trust sponsored by Digital Realty, with a market cap of $790.55 million.

Operations: The company's revenue is derived entirely from its commercial real estate investment trust segment, generating $69.54 million.

Estimated Discount To Fair Value: 48.7%

Digital Core REIT is trading at $0.63, significantly below its estimated fair value of $1.22, suggesting undervaluation based on cash flows. Despite a recent shareholder dilution and unstable dividend history, the REIT's forecasted earnings growth of 87.67% annually and expected profitability within three years highlight potential upside. Recent agreements to fully occupy its Toronto facility will enhance occupancy rates and generate approximately US$4.2 million in annual rent, bolstering revenue prospects further.

- Our expertly prepared growth report on Digital Core REIT implies its future financial outlook may be stronger than recent results.

- Click here and access our complete balance sheet health report to understand the dynamics of Digital Core REIT.

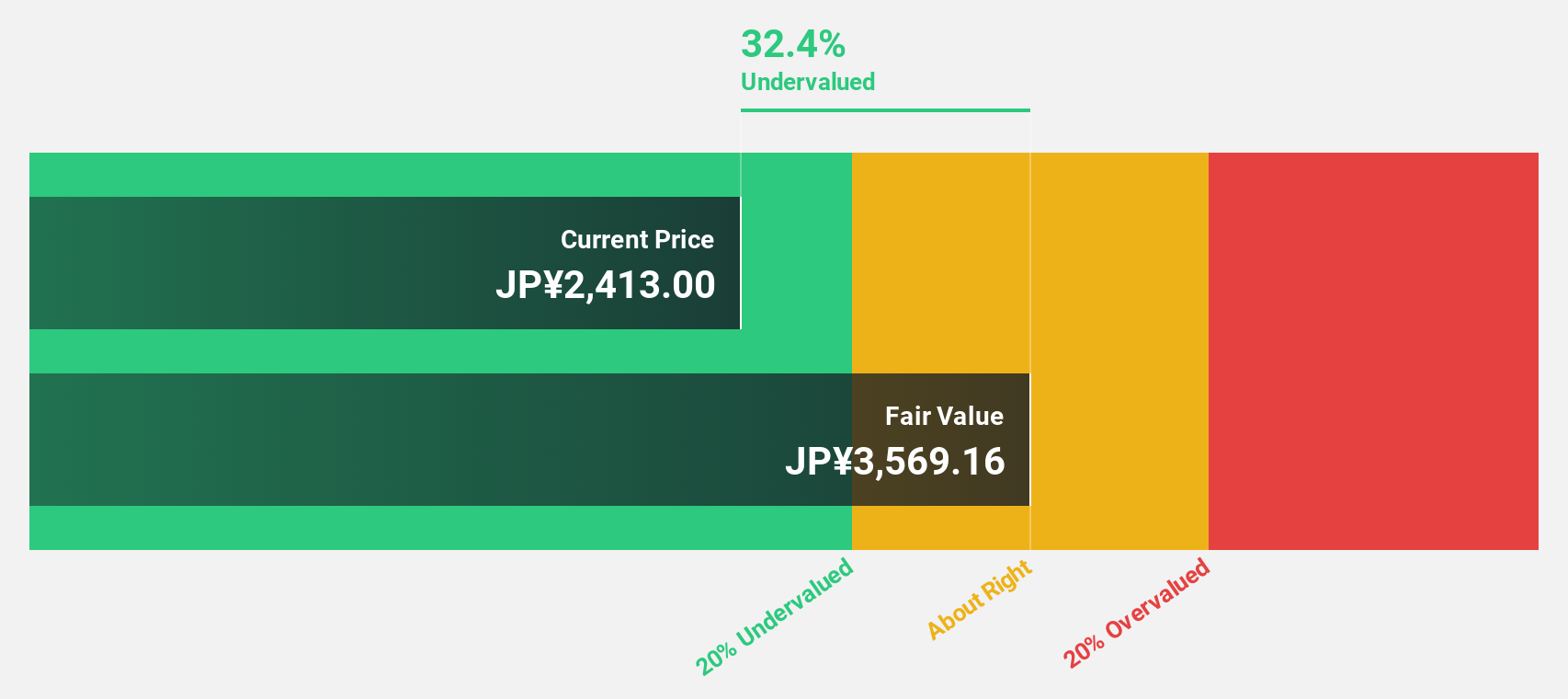

KATITAS (TSE:8919)

Overview: KATITAS CO., Ltd. operates in Japan by surveying, purchasing, refurbishing, remodeling, and selling used homes to individuals and families with a market cap of ¥163.82 billion.

Operations: The company's revenue segments include surveying, purchasing, refurbishing, remodeling, and selling pre-owned homes to individuals and families in Japan.

Estimated Discount To Fair Value: 37.5%

KATITAS is trading at ¥2,117, significantly below its estimated fair value of ¥3,388.97, highlighting potential undervaluation based on cash flows. Earnings grew by 76.9% last year and are forecasted to increase by 9.7% annually, outpacing the Japanese market average. Despite an unstable dividend history and recent removal from the FTSE All-World Index, a slight dividend increase to ¥28 per share reflects some positive momentum in shareholder returns.

- Our comprehensive growth report raises the possibility that KATITAS is poised for substantial financial growth.

- Click to explore a detailed breakdown of our findings in KATITAS' balance sheet health report.

Formycon (XTRA:FYB)

Overview: Formycon AG is a biotechnology company focused on developing biosimilar drugs in Germany and Switzerland, with a market cap of €844.88 million.

Operations: The company's revenue is primarily derived from its Drug Delivery Systems segment, which generated €60.80 million.

Estimated Discount To Fair Value: 44.7%

Formycon, trading at €47.85, is significantly undervalued compared to its estimated fair value of €86.49, with earnings expected to grow by 31.5% annually over the next three years, surpassing the German market's growth rate. Recent FDA approval for Otulfi enhances its biosimilar portfolio and revenue prospects. Despite past shareholder dilution and a low forecasted return on equity of 13.4%, analysts anticipate a substantial price increase of 79%.

- Upon reviewing our latest growth report, Formycon's projected financial performance appears quite optimistic.

- Dive into the specifics of Formycon here with our thorough financial health report.

Summing It All Up

- Delve into our full catalog of 914 Undervalued Stocks Based On Cash Flows here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:DCRU

Digital Core REIT

Digital Core REIT (SGX: DCRU) is a leading pure-play data centre REIT listed in Singapore and sponsored by Digital Realty, the largest global data centre owner and operator.

Reasonable growth potential average dividend payer.