Advertisement

- Germany

- /

- Healthtech

- /

- XTRA:COP

What You Can Learn From CompuGroup Medical SE & Co. KGaA's (ETR:COP) P/E After Its 34% Share Price Crash

Unfortunately for some shareholders, the CompuGroup Medical SE & Co. KGaA (ETR:COP) share price has dived 34% in the last thirty days, prolonging recent pain. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 66% loss during that time.

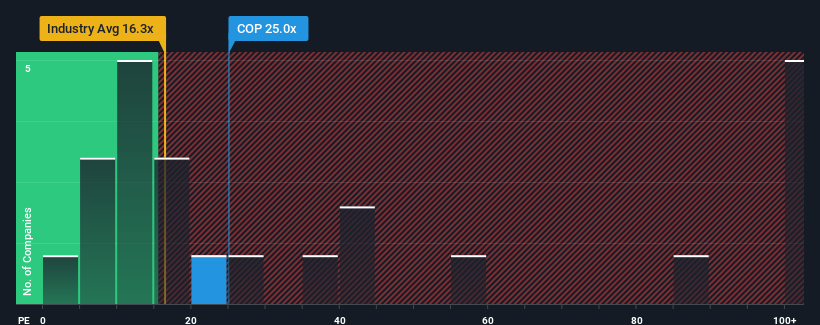

Even after such a large drop in price, given around half the companies in Germany have price-to-earnings ratios (or "P/E's") below 16x, you may still consider CompuGroup Medical SE KGaA as a stock to potentially avoid with its 25x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

CompuGroup Medical SE KGaA hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for CompuGroup Medical SE KGaA

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like CompuGroup Medical SE KGaA's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 63%. As a result, earnings from three years ago have also fallen 54% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 36% per annum during the coming three years according to the ten analysts following the company. With the market only predicted to deliver 14% per year, the company is positioned for a stronger earnings result.

In light of this, it's understandable that CompuGroup Medical SE KGaA's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From CompuGroup Medical SE KGaA's P/E?

CompuGroup Medical SE KGaA's P/E hasn't come down all the way after its stock plunged. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of CompuGroup Medical SE KGaA's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 4 warning signs for CompuGroup Medical SE KGaA (1 makes us a bit uncomfortable) you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:COP

CompuGroup Medical SE KGaA

Provides e-health services in Germany, Western and Eastern Europe, North America, and internationally.

Slight risk with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets