Advertisement

- Germany

- /

- Healthtech

- /

- XTRA:COP

Here's Why CompuGroup Medical SE KGaA (ETR:COP) Can Manage Its Debt Responsibly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that CompuGroup Medical SE & Co. KGaA (ETR:COP) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for CompuGroup Medical SE KGaA

What Is CompuGroup Medical SE KGaA's Debt?

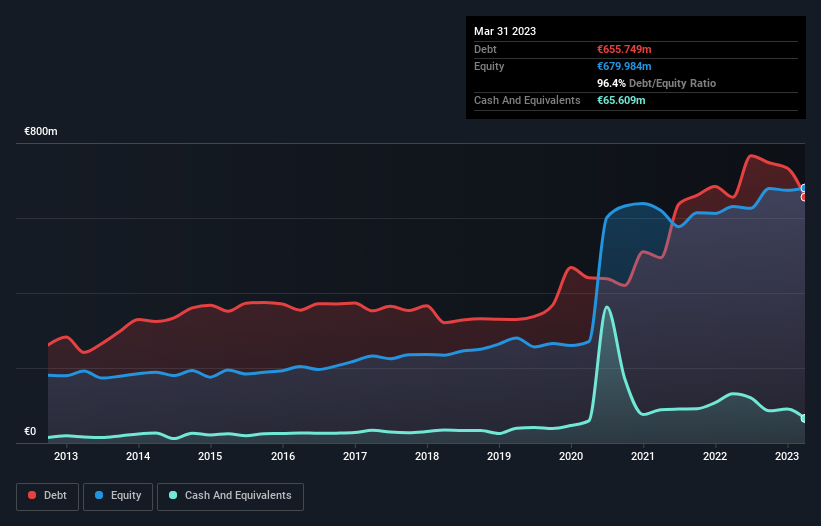

The chart below, which you can click on for greater detail, shows that CompuGroup Medical SE KGaA had €655.7m in debt in March 2023; about the same as the year before. On the flip side, it has €65.6m in cash leading to net debt of about €590.1m.

How Healthy Is CompuGroup Medical SE KGaA's Balance Sheet?

We can see from the most recent balance sheet that CompuGroup Medical SE KGaA had liabilities of €420.3m falling due within a year, and liabilities of €829.7m due beyond that. On the other hand, it had cash of €65.6m and €265.7m worth of receivables due within a year. So it has liabilities totalling €918.6m more than its cash and near-term receivables, combined.

This deficit isn't so bad because CompuGroup Medical SE KGaA is worth €2.42b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

CompuGroup Medical SE KGaA's debt is 3.7 times its EBITDA, and its EBIT cover its interest expense 4.3 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Notably, CompuGroup Medical SE KGaA's EBIT was pretty flat over the last year, which isn't ideal given the debt load. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if CompuGroup Medical SE KGaA can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, CompuGroup Medical SE KGaA generated free cash flow amounting to a very robust 86% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

When it comes to the balance sheet, the standout positive for CompuGroup Medical SE KGaA was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren't so heartening. For example, its net debt to EBITDA makes us a little nervous about its debt. We would also note that Healthcare Services industry companies like CompuGroup Medical SE KGaA commonly do use debt without problems. When we consider all the elements mentioned above, it seems to us that CompuGroup Medical SE KGaA is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 1 warning sign for CompuGroup Medical SE KGaA that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:COP

CompuGroup Medical SE KGaA

Provides e-health services in Germany, Western and Eastern Europe, North America, and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor