Advertisement

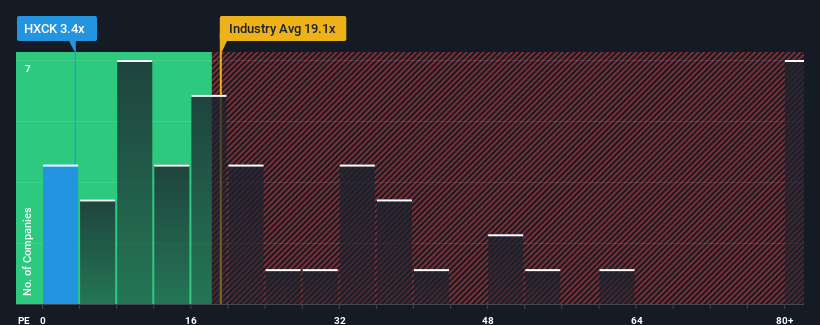

When close to half the companies in Germany have price-to-earnings ratios (or "P/E's") above 17x, you may consider Ernst Russ AG (ETR:HXCK) as a highly attractive investment with its 3.4x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Ernst Russ' earnings growth of late has been pretty similar to most other companies. It might be that many expect the mediocre earnings performance to degrade, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could pick up some stock while it's out of favour.

View our latest analysis for Ernst Russ

How Is Ernst Russ' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as depressed as Ernst Russ' is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered a decent 3.9% gain to the company's bottom line. The latest three year period has also seen an excellent 400% overall rise in EPS, aided somewhat by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 32% during the coming year according to the sole analyst following the company. Meanwhile, the broader market is forecast to expand by 19%, which paints a poor picture.

In light of this, it's understandable that Ernst Russ' P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Final Word

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Ernst Russ maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You should always think about risks. Case in point, we've spotted 2 warning signs for Ernst Russ you should be aware of, and 1 of them is concerning.

You might be able to find a better investment than Ernst Russ. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Ernst Russ might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:HXCK

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|10.6% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|26.4% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|35.4% undervalued

DZ

Community Contributor