- Germany

- /

- Construction

- /

- DB:3SQ1

AHT Syngas Technology N.V.'s (FRA:3SQ1) Stock Retreats 34% But Revenues Haven't Escaped The Attention Of Investors

AHT Syngas Technology N.V. (FRA:3SQ1) shareholders that were waiting for something to happen have been dealt a blow with a 34% share price drop in the last month. For any long-term shareholders, the last month ends a year to forget by locking in a 54% share price decline.

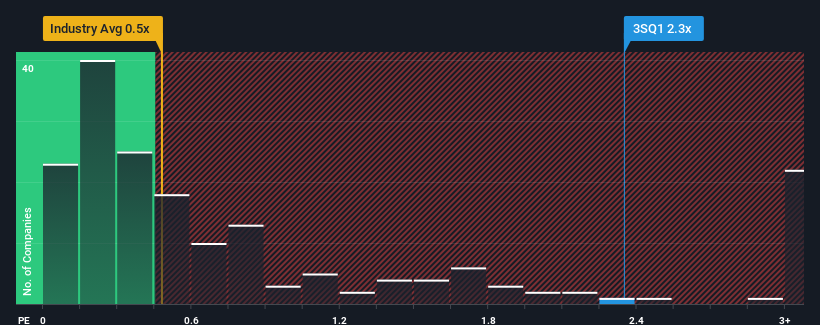

Even after such a large drop in price, when almost half of the companies in Germany's Construction industry have price-to-sales ratios (or "P/S") below 0.1x, you may still consider AHT Syngas Technology as a stock not worth researching with its 2.3x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for AHT Syngas Technology

How Has AHT Syngas Technology Performed Recently?

AHT Syngas Technology certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on AHT Syngas Technology will help you uncover what's on the horizon.Is There Enough Revenue Growth Forecasted For AHT Syngas Technology?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like AHT Syngas Technology's to be considered reasonable.

If we review the last year of revenue growth, we see the company's revenues grew exponentially. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 44% per annum over the next three years. With the industry only predicted to deliver 11% each year, the company is positioned for a stronger revenue result.

In light of this, it's understandable that AHT Syngas Technology's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

A significant share price dive has done very little to deflate AHT Syngas Technology's very lofty P/S. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that AHT Syngas Technology maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Construction industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for AHT Syngas Technology (of which 1 is a bit concerning!) you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DB:3SQ1

AHT Syngas Technology

Designs and installs biomass power plants worldwide.

Outstanding track record with excellent balance sheet.

Market Insights

Community Narratives