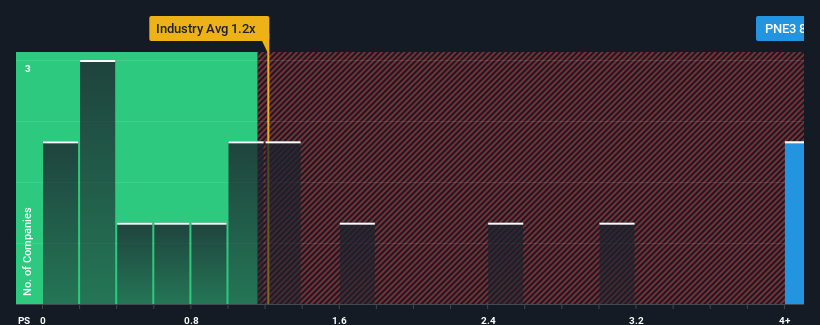

When you see that almost half of the companies in the Electrical industry in Germany have price-to-sales ratios (or "P/S") below 1.2x, PNE AG (ETR:PNE3) looks to be giving off strong sell signals with its 8.5x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for PNE

How Has PNE Performed Recently?

With only a limited decrease in revenue compared to most other companies of late, PNE has been doing relatively well. Perhaps the market is expecting the company to continue to outperform the industry, which has propped up the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price, especially if revenue continues to dissolve.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on PNE.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, PNE would need to produce outstanding growth that's well in excess of the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 11%. As a result, revenue from three years ago have also fallen 6.7% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the three analysts covering the company suggest revenue should grow by 27% per annum over the next three years. That's shaping up to be materially higher than the 9.8% per annum growth forecast for the broader industry.

With this information, we can see why PNE is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From PNE's P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look into PNE shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 1 warning sign for PNE that you need to be mindful of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:PNE3

PNE

Engages in the planning, construction, and operation of wind and photovoltaic (PV) farms and transformer stations in Germany and internationally.

Reasonable growth potential and slightly overvalued.