Advertisement

- China

- /

- Gas Utilities

- /

- SHSE:601139

Bearish: Analysts Just Cut Their Shenzhen Gas Corporation Ltd. (SHSE:601139) Revenue and EPS estimates

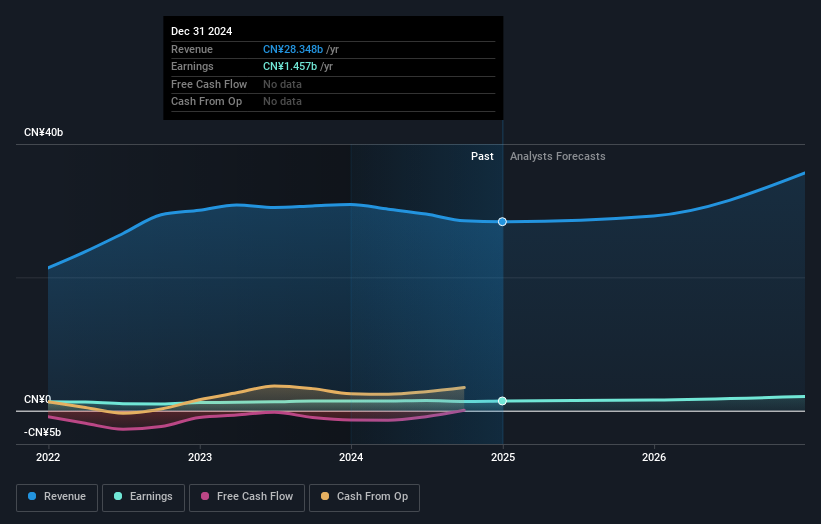

The analysts covering Shenzhen Gas Corporation Ltd. (SHSE:601139) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting analysts have soured majorly on the business.

Following the downgrade, the current consensus from Shenzhen Gas' five analysts is for revenues of CN¥29b in 2025 which - if met - would reflect a modest 3.0% increase on its sales over the past 12 months. Statutory earnings per share are presumed to increase 9.9% to CN¥0.56. Before this latest update, the analysts had been forecasting revenues of CN¥35b and earnings per share (EPS) of CN¥0.63 in 2025. Indeed, we can see that the analysts are a lot more bearish about Shenzhen Gas' prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for Shenzhen Gas

Despite the cuts to forecast earnings, there was no real change to the CN¥8.80 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Shenzhen Gas' revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 3.0% growth on an annualised basis. This is compared to a historical growth rate of 17% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 8.4% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Shenzhen Gas.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of Shenzhen Gas.

Unfortunately, the earnings downgrade - if accurate - may also place pressure on Shenzhen Gas' mountain of debt, which could lead to some belt tightening for shareholders. To see more of our financial analysis, you can click through to our free platform to learn more about its balance sheet and specific concerns we've identified.

You can also see our analysis of Shenzhen Gas' Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601139

Average dividend payer and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor