There's No Escaping CTS International Logistics Corporation Limited's (SHSE:603128) Muted Earnings

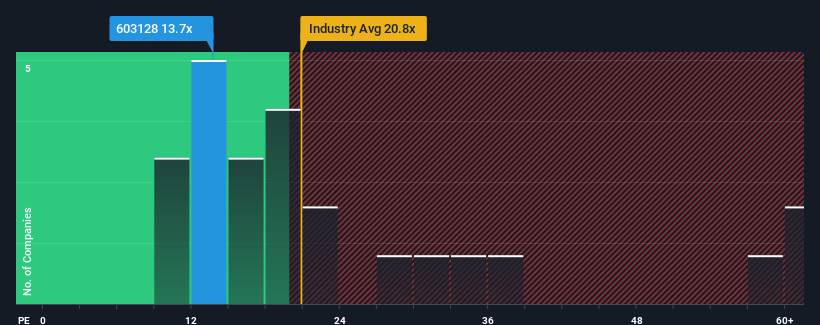

With a price-to-earnings (or "P/E") ratio of 13.7x CTS International Logistics Corporation Limited (SHSE:603128) may be sending very bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 37x and even P/E's higher than 70x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With earnings that are retreating more than the market's of late, CTS International Logistics has been very sluggish. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for CTS International Logistics

Is There Any Growth For CTS International Logistics?

The only time you'd be truly comfortable seeing a P/E as depressed as CTS International Logistics' is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered a frustrating 27% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 24% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Shifting to the future, estimates from the seven analysts covering the company suggest earnings should grow by 15% each year over the next three years. Meanwhile, the rest of the market is forecast to expand by 19% per year, which is noticeably more attractive.

With this information, we can see why CTS International Logistics is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On CTS International Logistics' P/E

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that CTS International Logistics maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Plus, you should also learn about this 1 warning sign we've spotted with CTS International Logistics.

If these risks are making you reconsider your opinion on CTS International Logistics, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603128

CTS International Logistics

A freight forwarding company, engages in the provision of logistics solutions globally.

Adequate balance sheet average dividend payer.

Market Insights

Community Narratives