Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SZSE:002456

OFILM Group Co., Ltd. Just Missed Earnings - But Analysts Have Updated Their Models

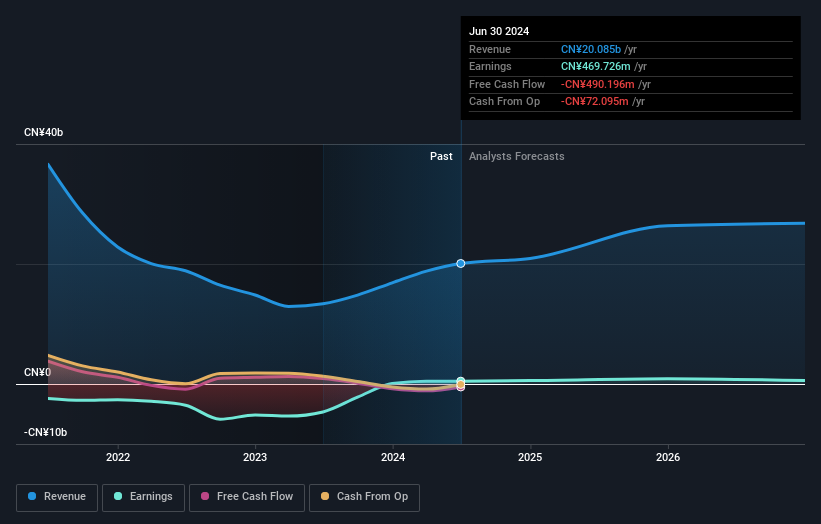

It's shaping up to be a tough period for OFILM Group Co., Ltd. (SZSE:002456), which a week ago released some disappointing second-quarter results that could have a notable impact on how the market views the stock. It looks like quite a negative result overall, with both revenues and earnings falling well short of analyst predictions. Revenues of CN¥4.9b missed by 19%, and statutory earnings per share of CN¥0.01 fell short of forecasts by 83%. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on OFILM Group after the latest results.

View our latest analysis for OFILM Group

Taking into account the latest results, the current consensus from OFILM Group's three analysts is for revenues of CN¥20.9b in 2024. This would reflect a satisfactory 4.2% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to leap 22% to CN¥0.17. Before this earnings report, the analysts had been forecasting revenues of CN¥22.4b and earnings per share (EPS) of CN¥0.20 in 2024. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a real cut to earnings per share numbers.

The analysts made no major changes to their price target of CN¥8.25, suggesting the downgrades are not expected to have a long-term impact on OFILM Group's valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on OFILM Group, with the most bullish analyst valuing it at CN¥12.14 and the most bearish at CN¥6.10 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. One thing stands out from these estimates, which is that OFILM Group is forecast to grow faster in the future than it has in the past, with revenues expected to display 8.5% annualised growth until the end of 2024. If achieved, this would be a much better result than the 30% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 18% annually for the foreseeable future. Although OFILM Group's revenues are expected to improve, it seems that the analysts are still bearish on the business, forecasting it to grow slower than the broader industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for OFILM Group. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. The consensus price target held steady at CN¥8.25, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple OFILM Group analysts - going out to 2026, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for OFILM Group (1 is a bit unpleasant) you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002456

OFILM Group

Engages in the development, production, and operation of optoelectronic devices, system equipment, network, communication components, electronic special equipment, and instruments in China and internationally.

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.1% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|15.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor