Top Growth Companies With Strong Insider Ownership February 2025

Reviewed by Simply Wall St

As global markets navigate a landscape marked by fluctuating corporate earnings and geopolitical uncertainties, investors are closely watching the Federal Reserve's steady interest rate policy alongside competitive pressures in the AI sector. Amid this backdrop, identifying growth companies with high insider ownership can offer insights into potential resilience and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.9% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Pharma Mar (BME:PHM) | 11.9% | 44.7% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 86% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Findi (ASX:FND) | 35.8% | 110.7% |

Below we spotlight a couple of our favorites from our exclusive screener.

Jiangyin Jianghua Microelectronics Materials (SHSE:603078)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangyin Jianghua Microelectronics Materials Co., Ltd specializes in manufacturing and supplying wet electronic chemicals for microelectronics and optoelectronics in China, with a market cap of CN¥6.28 billion.

Operations: The company's revenue segments are focused on the production and distribution of wet electronic chemicals tailored for the microelectronics and optoelectronics sectors within China.

Insider Ownership: 20.8%

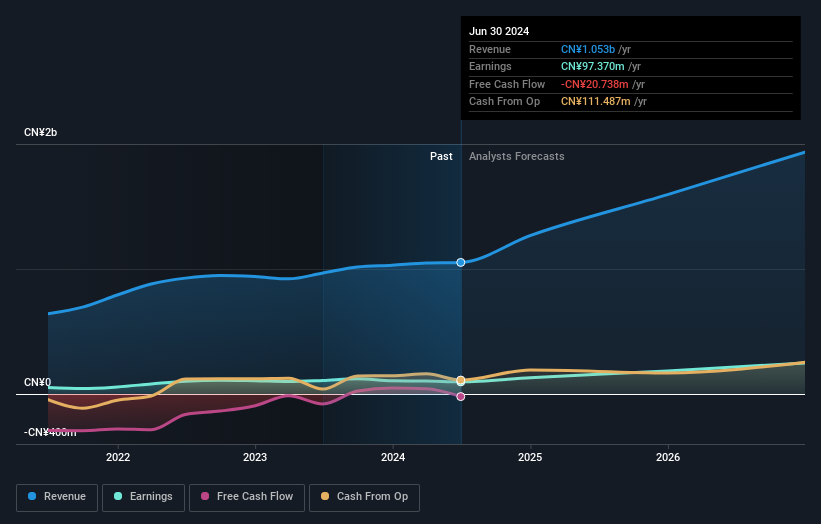

Jiangyin Jianghua Microelectronics Materials is poised for significant growth, with earnings projected to increase by 38.7% annually, outpacing the Chinese market's 25.1%. Revenue is also set to expand at a robust 25.1% per year, surpassing both market and high-growth benchmarks. Despite this potential, the company's share price has been highly volatile recently, and its forecasted return on equity remains modest at 11.2%. No substantial insider trading activity has been reported in recent months.

- Click here to discover the nuances of Jiangyin Jianghua Microelectronics Materials with our detailed analytical future growth report.

- The analysis detailed in our Jiangyin Jianghua Microelectronics Materials valuation report hints at an inflated share price compared to its estimated value.

Appotronics (SHSE:688007)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Appotronics Corporation Limited is involved in the research, development, production, sale, and leasing of laser display devices and machines in China with a market cap of CN¥6.54 billion.

Operations: Appotronics generates revenue through its activities in research, development, production, sales, and leasing of laser display devices and machines within China.

Insider Ownership: 23.2%

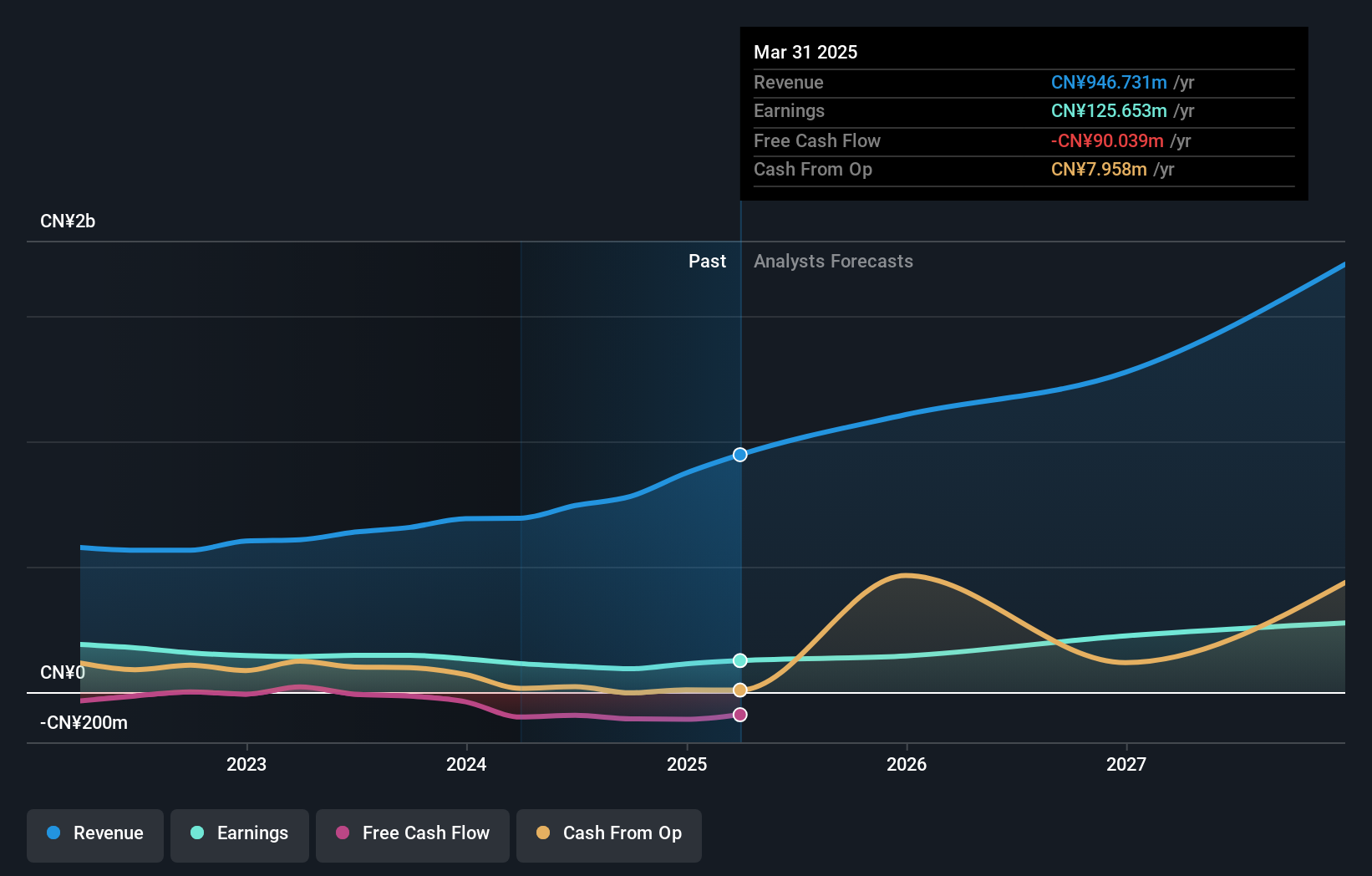

Appotronics is positioned for growth, with earnings expected to rise significantly at 90.1% annually, surpassing the Chinese market's average. Revenue growth is also projected at 21.5% per year, outpacing market trends. Despite a recent decline in profit margins and low forecasted return on equity (8.7%), the company trades below its estimated fair value by 15.8%. The recent partnership with Ceres Holographics aims to enhance their automotive display solutions, potentially expanding Appotronics' market reach.

- Get an in-depth perspective on Appotronics' performance by reading our analyst estimates report here.

- The analysis detailed in our Appotronics valuation report hints at an deflated share price compared to its estimated value.

Cubic Sensor and InstrumentLtd (SHSE:688665)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Cubic Sensor and Instrument Co., Ltd. manufactures gas sensors and sensor solutions in China, with a market cap of CN¥3.38 billion.

Operations: Cubic Sensor and Instrument Co., Ltd. generates revenue from its gas sensors and sensor solutions business in China.

Insider Ownership: 10.6%

Cubic Sensor and Instrument Ltd. is poised for robust growth, with earnings projected to grow 42% annually, outpacing the Chinese market. Revenue is expected to increase at 20.6% per year, surpassing market averages. Despite a volatile share price and declining profit margins from last year (22.3% to 11.9%), the stock trades at a favorable price-to-earnings ratio of 39.6x compared to industry peers, offering good relative value for investors seeking growth opportunities.

- Click here and access our complete growth analysis report to understand the dynamics of Cubic Sensor and InstrumentLtd.

- In light of our recent valuation report, it seems possible that Cubic Sensor and InstrumentLtd is trading behind its estimated value.

Turning Ideas Into Actions

- Gain an insight into the universe of 1479 Fast Growing Companies With High Insider Ownership by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603078

Jiangyin Jianghua Microelectronics Materials

Manufactures and supplies wet electronic chemicals for microelectronics and optoelectronics in China.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives