- China

- /

- Electronic Equipment and Components

- /

- SHSE:688100

Global Growth Stocks Insiders Are Betting On

Reviewed by Simply Wall St

As global markets face headwinds from economic uncertainty, inflation fears, and trade policy challenges, investors are increasingly cautious about growth prospects. Despite these concerns, stocks with high insider ownership can be appealing as insiders may have confidence in the company's long-term potential even amid market volatility.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 24.7% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Pharma Mar (BME:PHM) | 11.8% | 40.8% |

| Vow (OB:VOW) | 13.1% | 111.2% |

| Laopu Gold (SEHK:6181) | 36.4% | 30.9% |

| CD Projekt (WSE:CDR) | 29.7% | 36.8% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| Nordic Halibut (OB:NOHAL) | 29.8% | 56.3% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

Let's explore several standout options from the results in the screener.

DigiPlus Interactive (PSE:PLUS)

Simply Wall St Growth Rating: ★★★★★★

Overview: DigiPlus Interactive Corp. operates general amusement, recreation enterprises, hotels, and gaming facilities in the Philippines with a market cap of ₱159.12 billion.

Operations: The company's revenue segments include the Casino Group with ₱501.05 million, the Retail Group generating ₱61.84 billion, the Property Group contributing ₱82.19 million, and the Network and License Group with ₱402.91 million in revenue.

Insider Ownership: 11.3%

Revenue Growth Forecast: 22.2% p.a.

DigiPlus Interactive is expanding its international presence with the establishment of DigiPlus Global in Singapore, focusing on strategic partnerships and talent acquisition. Despite significant insider selling recently, the company maintains strong growth prospects with forecasted annual revenue growth of 22.2% and earnings growth of 27.5%, both outpacing the Philippine market averages. Trading at a substantial discount to estimated fair value, DigiPlus offers compelling relative value compared to peers in digital entertainment.

- Delve into the full analysis future growth report here for a deeper understanding of DigiPlus Interactive.

- The valuation report we've compiled suggests that DigiPlus Interactive's current price could be quite moderate.

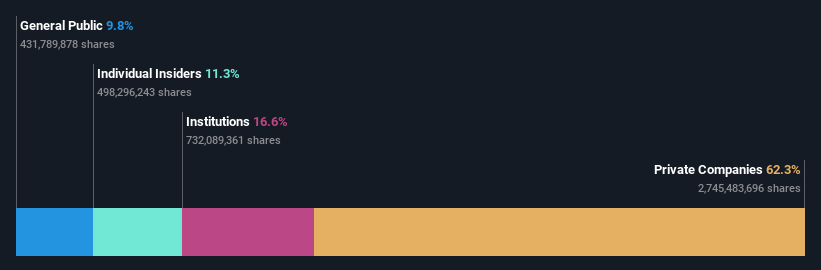

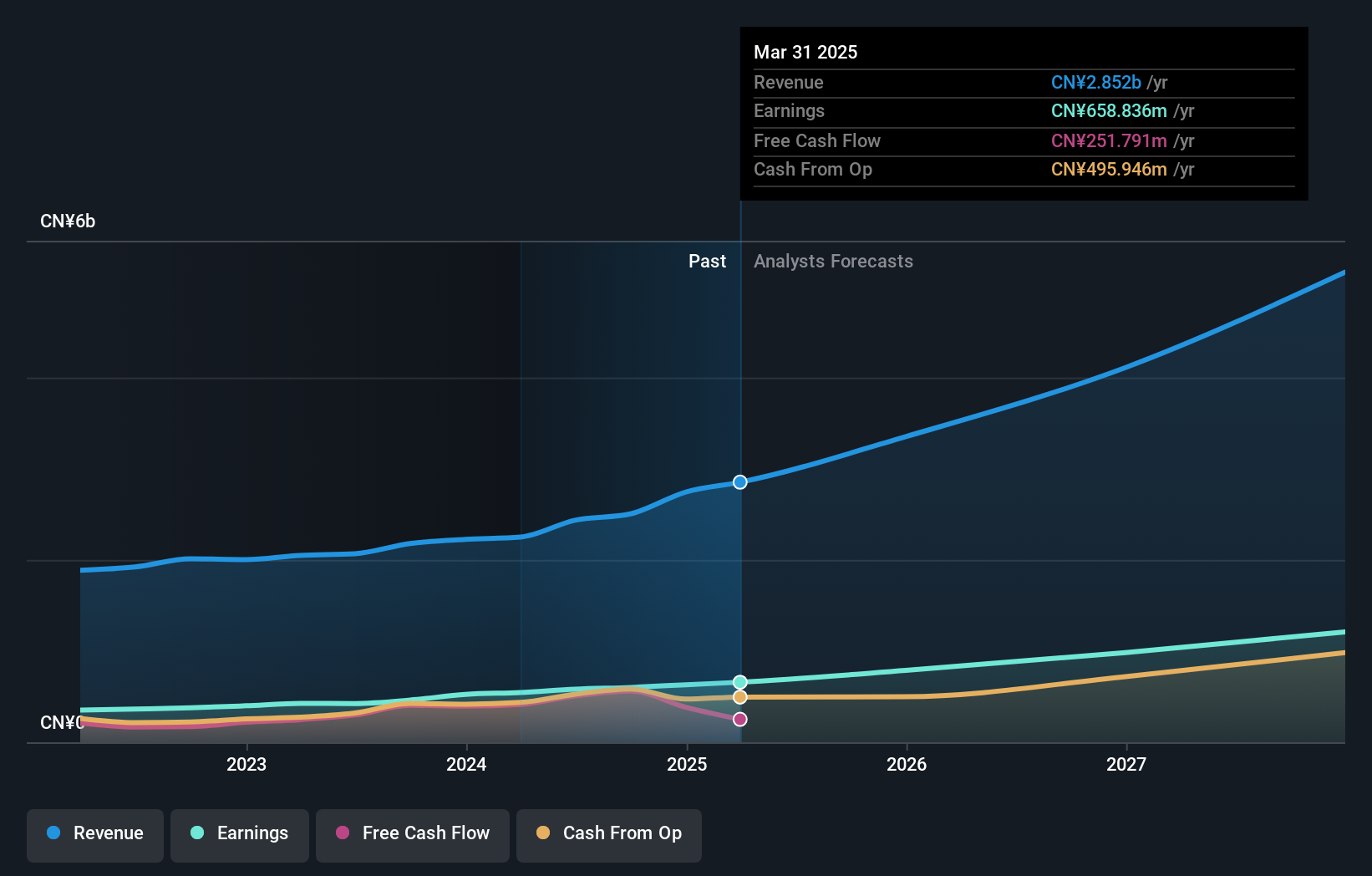

Willfar Information Technology (SHSE:688100)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Willfar Information Technology Co., Ltd. offers smart utility services and IoT solutions both in China and internationally, with a market cap of CN¥18.37 billion.

Operations: The company's revenue segments include Communication Module (CN¥776.32 million), Communications Gateway (CN¥746.82 million), Electric Monitoring Terminal (CN¥833.16 million), Smart Utility Management System (CN¥148.13 million), and Water Vapor Heat Sensing Terminal (CN¥230.05 million).

Insider Ownership: 21.5%

Revenue Growth Forecast: 19.3% p.a.

Willfar Information Technology's earnings and revenue have shown robust growth, with a 20.1% increase in earnings last year and forecasts predicting a 20.49% annual growth rate for the future. Although insider trading information is limited, the company has initiated a share buyback program worth up to CNY 150 million, enhancing shareholder value. Trading below market P/E ratios, Willfar offers good relative value despite its slower projected revenue growth compared to China's market average.

- Click here and access our complete growth analysis report to understand the dynamics of Willfar Information Technology.

- According our valuation report, there's an indication that Willfar Information Technology's share price might be on the cheaper side.

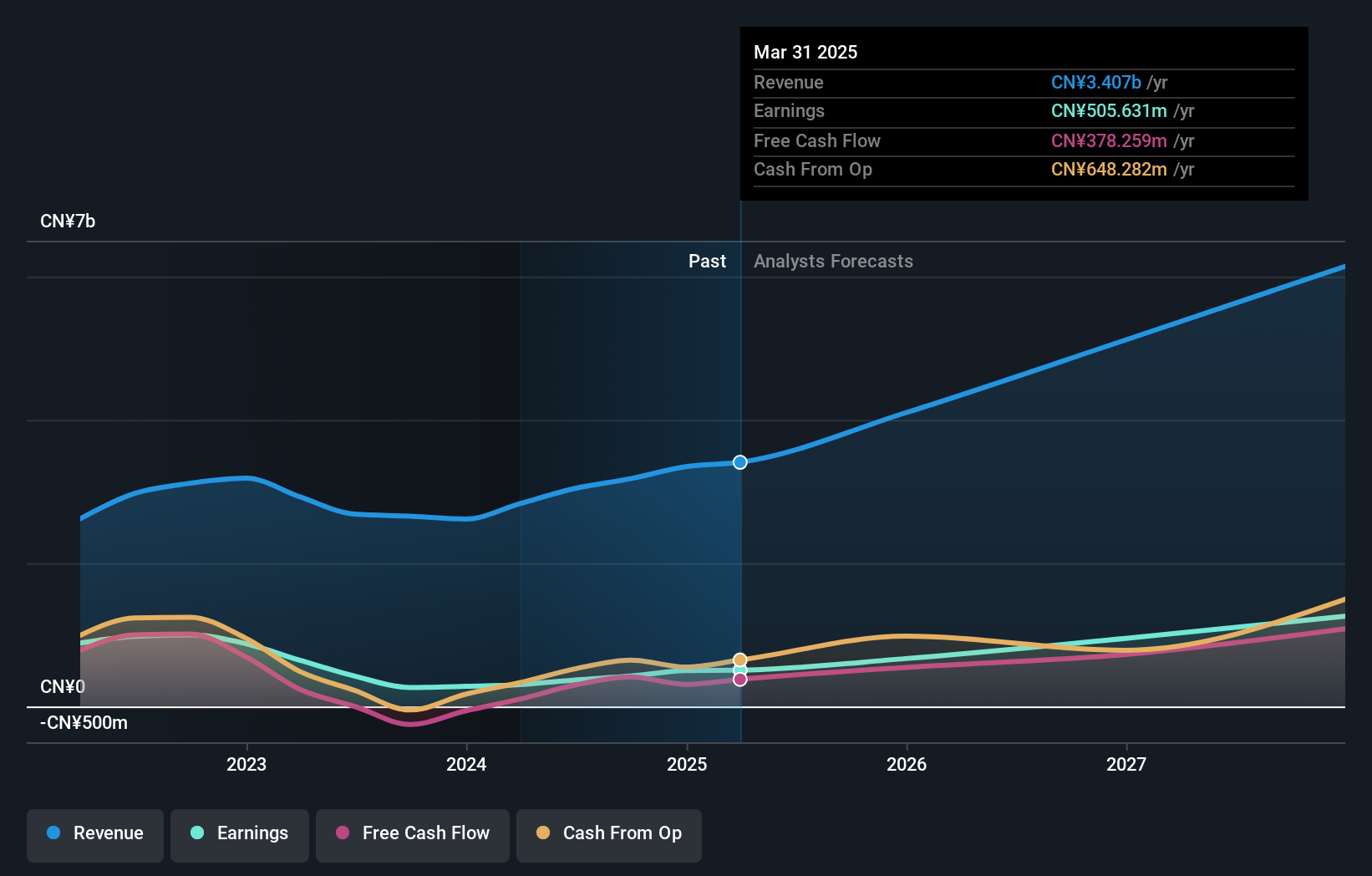

SG Micro (SZSE:300661)

Simply Wall St Growth Rating: ★★★★★☆

Overview: SG Micro Corp designs, markets, and sells analog ICs primarily in China, with a market cap of CN¥41.60 billion.

Operations: The company generates revenue of CN¥3.18 billion from its operations in the Integrated Circuit Industry.

Insider Ownership: 32.9%

Revenue Growth Forecast: 22% p.a.

SG Micro's earnings are forecast to grow significantly at 40.33% per year, outpacing the CN market average of 24.6%, with revenue expected to increase by 22% annually, surpassing the market's 13.1%. Despite recent share price volatility and low projected return on equity of 16.2%, its strong historical growth—59.9% earnings increase last year—demonstrates potential for continued expansion without substantial insider trading activity recently observed.

- Take a closer look at SG Micro's potential here in our earnings growth report.

- Our valuation report here indicates SG Micro may be overvalued.

Key Takeaways

- Get an in-depth perspective on all 908 Fast Growing Global Companies With High Insider Ownership by using our screener here.

- Seeking Other Investments? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Willfar Information Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688100

Willfar Information Technology

Provides smart utility services and IoT solutions in China and internationally.

Flawless balance sheet and good value.

Market Insights

Community Narratives