- China

- /

- Electrical

- /

- SZSE:002606

Top Chinese Growth Companies With High Insider Ownership For September 2024

Reviewed by Simply Wall St

As global markets grapple with economic uncertainties, Chinese equities have seen notable declines, reflecting weak corporate earnings and mixed economic data. Amid this backdrop, identifying growth companies with high insider ownership can be particularly appealing, as such ownership often signals confidence in the company's future prospects and alignment of interests between insiders and investors.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 18% | 28.7% |

| Jiayou International LogisticsLtd (SHSE:603871) | 22.6% | 24.6% |

| Western Regions Tourism DevelopmentLtd (SZSE:300859) | 13.9% | 39.2% |

| Arctech Solar Holding (SHSE:688408) | 38.6% | 29.9% |

| Quick Intelligent EquipmentLtd (SHSE:603203) | 34.4% | 33.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 67.5% |

| UTour Group (SZSE:002707) | 23% | 28.7% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 41.7% |

| BIWIN Storage Technology (SHSE:688525) | 18.8% | 116.8% |

| Offcn Education Technology (SZSE:002607) | 25.1% | 75.7% |

Let's dive into some prime choices out of the screener.

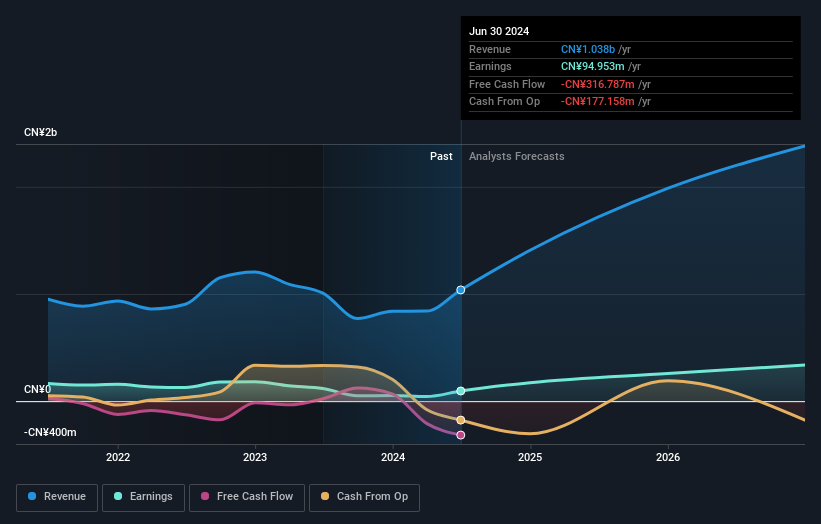

Dalian Insulator Group (SZSE:002606)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Dalian Insulator Group Co., Ltd, with a market cap of CN¥3.69 billion, engages in the research, development, manufacture, and sale of porcelain insulators both in China and internationally.

Operations: Revenue Segments (in millions of CN¥): #start# Dalian Insulator Group Co., Ltd, together with its subsidiaries, engages in the research, development, manufacture, and sale of porcelain insulators in China and internationally.Market Cap:CN¥3691399531Revenue Segments (in millions of CN¥):null #end# The company's revenue segments include the domestic market in China and international sales.

Insider Ownership: 13%

Earnings Growth Forecast: 43.4% p.a.

Dalian Insulator Group shows promising growth potential with forecasted earnings and revenue growth rates of 43.38% and 31.4% per year, respectively, outpacing the broader Chinese market. The company reported significant financial improvements for the first half of 2024, with net income rising to CNY 79.04 million from CNY 36.43 million a year ago. Additionally, insider ownership remains high without substantial selling over the past three months, indicating strong internal confidence in future performance.

- Click here to discover the nuances of Dalian Insulator Group with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of Dalian Insulator Group shares in the market.

Eaglerise Electric & Electronic (China) (SZSE:002922)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Eaglerise Electric & Electronic (China) Co., Ltd. (SZSE:002922) operates in the electrical and electronic manufacturing sector with a market cap of CN¥7.37 billion.

Operations: Eaglerise Electric & Electronic (China) Co., Ltd. generates revenue from multiple segments within the electrical and electronic manufacturing sector.

Insider Ownership: 32.2%

Earnings Growth Forecast: 29.5% p.a.

Eaglerise Electric & Electronic (China) has demonstrated strong growth, with half-year sales rising to CNY 2.05 billion from CNY 1.57 billion and net income increasing to CNY 176.3 million from CNY 90.23 million year-over-year. Despite a highly volatile share price, the company is trading at a significant discount to its estimated fair value and boasts high insider ownership with no recent substantial selling, suggesting internal confidence in its future performance amidst forecasted robust revenue and earnings growth rates of over 26% annually.

- Navigate through the intricacies of Eaglerise Electric & Electronic (China) with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Eaglerise Electric & Electronic (China)'s shares may be trading at a discount.

Jolywood (Suzhou) SunwattLtd (SZSE:300393)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jolywood (Suzhou) Sunwatt Co., Ltd. manufactures and sells integrated photovoltaic (PV) products worldwide, with a market cap of CN¥5.93 billion.

Operations: The company generates revenue primarily from the photovoltaic industry, amounting to CN¥9.58 billion.

Insider Ownership: 19.4%

Earnings Growth Forecast: 70.1% p.a.

Jolywood (Suzhou) Sunwatt Ltd. is forecasted to achieve significant revenue growth of 26.8% per year, outpacing the Chinese market average. Despite recent financial setbacks, including a net loss of CNY 305.88 million for H1 2024 and a substantial drop in revenue compared to the previous year, the company is expected to become profitable within three years. High insider ownership indicates strong internal confidence despite current challenges and low return on equity projections.

- Delve into the full analysis future growth report here for a deeper understanding of Jolywood (Suzhou) SunwattLtd.

- According our valuation report, there's an indication that Jolywood (Suzhou) SunwattLtd's share price might be on the cheaper side.

Where To Now?

- Investigate our full lineup of 378 Fast Growing Chinese Companies With High Insider Ownership right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002606

Dalian Insulator Group

Engages in the research, development, manufacture, and sale of porcelain insulators in China and internationally.

High growth potential with proven track record.