- China

- /

- Semiconductors

- /

- SZSE:300393

Investors Will Want Jolywood (Suzhou) Sunwatt's (SZSE:300393) Growth In ROCE To Persist

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So when we looked at Jolywood (Suzhou) Sunwatt (SZSE:300393) and its trend of ROCE, we really liked what we saw.

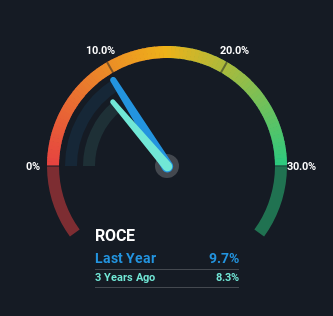

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Jolywood (Suzhou) Sunwatt:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.097 = CN¥852m ÷ (CN¥18b - CN¥9.4b) (Based on the trailing twelve months to September 2023).

So, Jolywood (Suzhou) Sunwatt has an ROCE of 9.7%. On its own that's a low return, but compared to the average of 5.3% generated by the Semiconductor industry, it's much better.

View our latest analysis for Jolywood (Suzhou) Sunwatt

In the above chart we have measured Jolywood (Suzhou) Sunwatt's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Jolywood (Suzhou) Sunwatt .

So How Is Jolywood (Suzhou) Sunwatt's ROCE Trending?

Even though ROCE is still low in absolute terms, it's good to see it's heading in the right direction. The data shows that returns on capital have increased substantially over the last five years to 9.7%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 131%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Essentially the business now has suppliers or short-term creditors funding about 52% of its operations, which isn't ideal. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

In Conclusion...

In summary, it's great to see that Jolywood (Suzhou) Sunwatt can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. And with a respectable 68% awarded to those who held the stock over the last five years, you could argue that these developments are starting to get the attention they deserve. Therefore, we think it would be worth your time to check if these trends are going to continue.

Jolywood (Suzhou) Sunwatt does have some risks though, and we've spotted 2 warning signs for Jolywood (Suzhou) Sunwatt that you might be interested in.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300393

Jolywood (Suzhou) SunwattLtd

Manufactures and sells integrated photovoltaic (PV) products worldwide.

Slightly overvalued very low.

Market Insights

Community Narratives