Advertisement

- China

- /

- Semiconductors

- /

- SZSE:002185

Here's Why Tianshui Huatian Technology (SZSE:002185) Has A Meaningful Debt Burden

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Tianshui Huatian Technology Co., Ltd. (SZSE:002185) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Tianshui Huatian Technology's Debt?

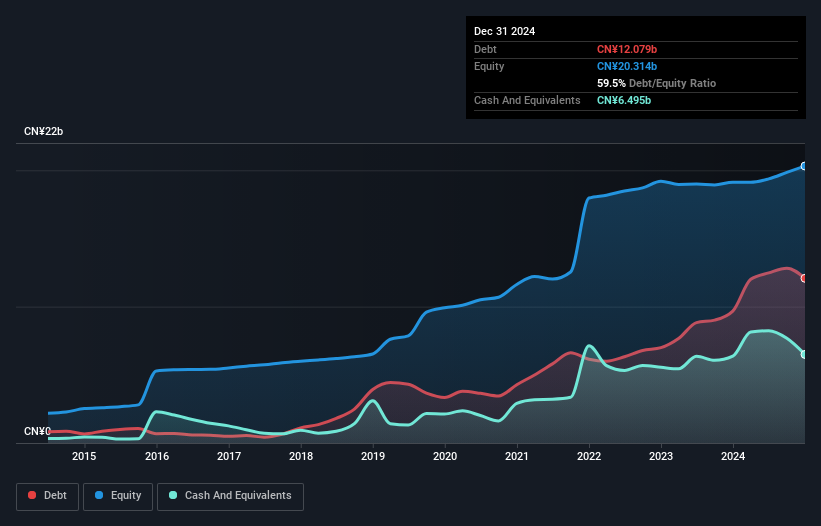

As you can see below, at the end of December 2024, Tianshui Huatian Technology had CN¥12.1b of debt, up from CN¥9.67b a year ago. Click the image for more detail. However, because it has a cash reserve of CN¥6.50b, its net debt is less, at about CN¥5.58b.

How Healthy Is Tianshui Huatian Technology's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Tianshui Huatian Technology had liabilities of CN¥9.86b due within 12 months and liabilities of CN¥8.06b due beyond that. Offsetting these obligations, it had cash of CN¥6.50b as well as receivables valued at CN¥2.68b due within 12 months. So it has liabilities totalling CN¥8.74b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Tianshui Huatian Technology is worth CN¥33.9b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

See our latest analysis for Tianshui Huatian Technology

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

We'd say that Tianshui Huatian Technology's moderate net debt to EBITDA ratio ( being 1.8), indicates prudence when it comes to debt. And its commanding EBIT of 1k times its interest expense, implies the debt load is as light as a peacock feather. Although Tianshui Huatian Technology made a loss at the EBIT level, last year, it was also good to see that it generated CN¥560m in EBIT over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Tianshui Huatian Technology's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Tianshui Huatian Technology saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Neither Tianshui Huatian Technology's ability to convert EBIT to free cash flow nor its EBIT growth rate gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that Tianshui Huatian Technology is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. Over time, share prices tend to follow earnings per share, so if you're interested in Tianshui Huatian Technology, you may well want to click here to check an interactive graph of its earnings per share history.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Tianshui Huatian Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002185

Tianshui Huatian Technology

Engages in research, development, production, packaging, testing, and sales of semiconductor integrated circuits in China and internationally.

Adequate balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor