- China

- /

- Semiconductors

- /

- SZSE:002049

Further Upside For Unigroup Guoxin Microelectronics Co., Ltd. (SZSE:002049) Shares Could Introduce Price Risks After 33% Bounce

Unigroup Guoxin Microelectronics Co., Ltd. (SZSE:002049) shareholders are no doubt pleased to see that the share price has bounced 33% in the last month, although it is still struggling to make up recently lost ground. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 34% over that time.

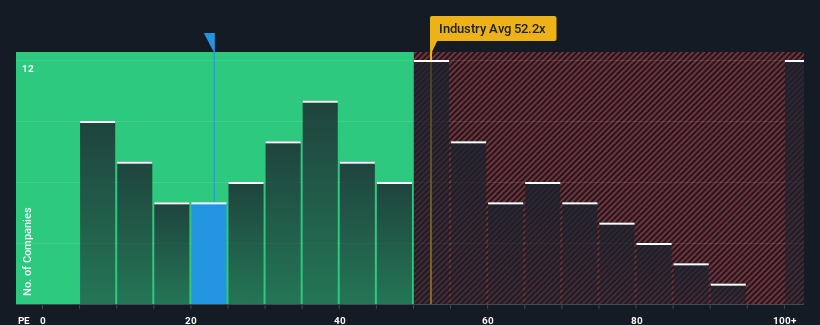

In spite of the firm bounce in price, Unigroup Guoxin Microelectronics may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 23x, since almost half of all companies in China have P/E ratios greater than 29x and even P/E's higher than 53x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Unigroup Guoxin Microelectronics certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Unigroup Guoxin Microelectronics

Does Growth Match The Low P/E?

Unigroup Guoxin Microelectronics' P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

If we review the last year of earnings growth, the company posted a worthy increase of 3.6%. The latest three year period has also seen an excellent 264% overall rise in EPS, aided somewhat by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 39% during the coming year according to the seven analysts following the company. With the market predicted to deliver 41% growth , the company is positioned for a comparable earnings result.

In light of this, it's peculiar that Unigroup Guoxin Microelectronics' P/E sits below the majority of other companies. It may be that most investors are not convinced the company can achieve future growth expectations.

The Final Word

Despite Unigroup Guoxin Microelectronics' shares building up a head of steam, its P/E still lags most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Unigroup Guoxin Microelectronics currently trades on a lower than expected P/E since its forecast growth is in line with the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Unigroup Guoxin Microelectronics with six simple checks will allow you to discover any risks that could be an issue.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002049

Unigroup Guoxin Microelectronics

Unigroup Guoxin Microelectronics Co., Ltd.

Flawless balance sheet with high growth potential and pays a dividend.

Market Insights

Community Narratives