Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688591

Telink Semiconductor(Shanghai)Co.,Ltd. (SHSE:688591) Stock Rockets 28% As Investors Are Less Pessimistic Than Expected

Despite an already strong run, Telink Semiconductor(Shanghai)Co.,Ltd. (SHSE:688591) shares have been powering on, with a gain of 28% in the last thirty days. The last month tops off a massive increase of 110% in the last year.

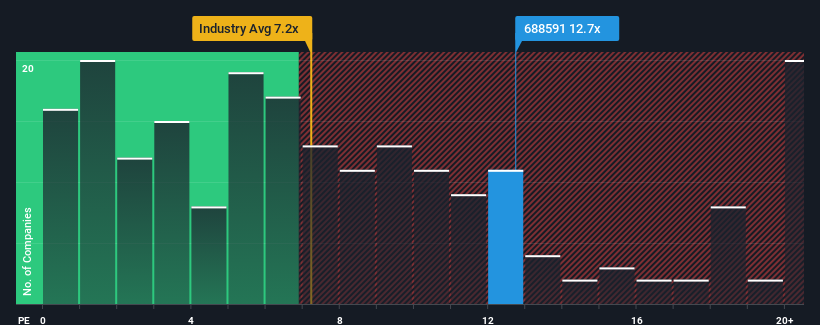

Since its price has surged higher, Telink Semiconductor(Shanghai)Co.Ltd may be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 12.7x, since almost half of all companies in the Semiconductor industry in China have P/S ratios under 7.2x and even P/S lower than 3x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for Telink Semiconductor(Shanghai)Co.Ltd

How Has Telink Semiconductor(Shanghai)Co.Ltd Performed Recently?

With revenue growth that's superior to most other companies of late, Telink Semiconductor(Shanghai)Co.Ltd has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Telink Semiconductor(Shanghai)Co.Ltd's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as steep as Telink Semiconductor(Shanghai)Co.Ltd's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 33% gain to the company's top line. Revenue has also lifted 30% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 33% over the next year. That's shaping up to be materially lower than the 44% growth forecast for the broader industry.

With this in consideration, we believe it doesn't make sense that Telink Semiconductor(Shanghai)Co.Ltd's P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Final Word

Shares in Telink Semiconductor(Shanghai)Co.Ltd have seen a strong upwards swing lately, which has really helped boost its P/S figure. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've concluded that Telink Semiconductor(Shanghai)Co.Ltd currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Telink Semiconductor(Shanghai)Co.Ltd you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Telink Semiconductor(Shanghai)Co.Ltd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688591

Telink Semiconductor(Shanghai)Co.Ltd

Engages in research, development, design, and sales of low-power wireless IoT chips.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor