Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688516

Investors Still Aren't Entirely Convinced By Wuxi Autowell Technology Co.,Ltd.'s (SHSE:688516) Earnings Despite 27% Price Jump

Wuxi Autowell Technology Co.,Ltd. (SHSE:688516) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 30% in the last twelve months.

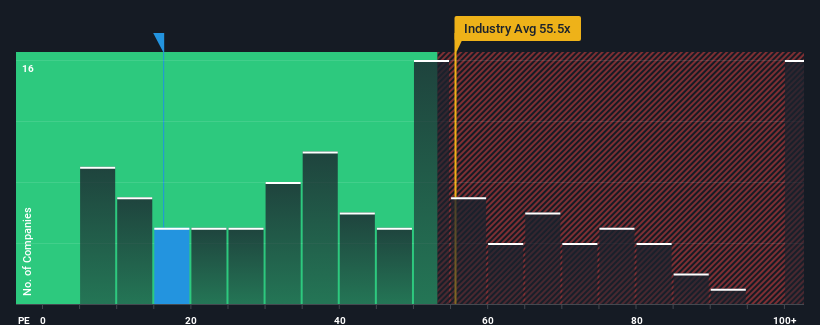

Although its price has surged higher, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 30x, you may still consider Wuxi Autowell TechnologyLtd as an attractive investment with its 16.2x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Wuxi Autowell TechnologyLtd certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Wuxi Autowell TechnologyLtd

How Is Wuxi Autowell TechnologyLtd's Growth Trending?

There's an inherent assumption that a company should underperform the market for P/E ratios like Wuxi Autowell TechnologyLtd's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 66% gain to the company's bottom line. The latest three year period has also seen an excellent 570% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 52% during the coming year according to the nine analysts following the company. That's shaping up to be materially higher than the 41% growth forecast for the broader market.

In light of this, it's peculiar that Wuxi Autowell TechnologyLtd's P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Final Word

Wuxi Autowell TechnologyLtd's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Wuxi Autowell TechnologyLtd currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Before you take the next step, you should know about the 1 warning sign for Wuxi Autowell TechnologyLtd that we have uncovered.

If these risks are making you reconsider your opinion on Wuxi Autowell TechnologyLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Wuxi Autowell TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688516

Wuxi Autowell TechnologyLtd

Manufactures and sells automation equipment for photovoltaic equipment, lithium battery equipment, and semiconductor industries in China.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|1.4% undervalued

RO

Community Contributor