- China

- /

- Semiconductors

- /

- SHSE:603501

3 Growth Companies With High Insider Ownership And 13% Revenue Growth

Reviewed by Simply Wall St

Global markets have shown resilience recently, with U.S. stocks rebounding after a significant sell-off and growth stocks outperforming value shares, driven by strong performances in the technology sector. Amidst these market dynamics, insider ownership can be a valuable indicator of confidence in a company's long-term prospects. In this context, identifying growth companies with high insider ownership and notable revenue growth can offer unique insights into potential investment opportunities.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.5% | 52.1% |

| Medley (TSE:4480) | 34% | 30.4% |

| KebNi (OM:KEBNI B) | 37.8% | 86.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 95% |

| Adocia (ENXTPA:ADOC) | 11.9% | 63% |

| Adveritas (ASX:AV1) | 21.1% | 144.2% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 100.3% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

Below we spotlight a couple of our favorites from our exclusive screener.

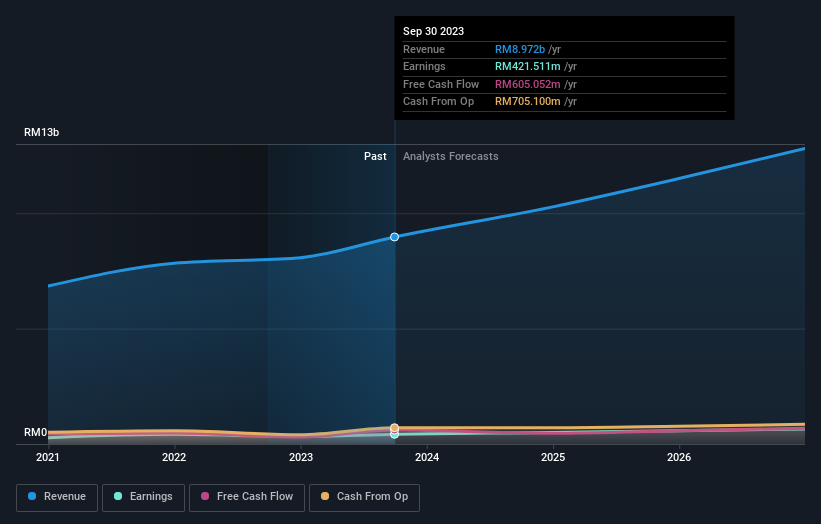

99 Speed Mart Retail Holdings Berhad (KLSE:99SMART)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: 99 Speed Mart Retail Holdings Berhad, an investment holding company with a market cap of MYR15.96 billion, operates mini supermarkets in Malaysia.

Operations: Revenue from department stores amounts to MYR8.97 billion.

Insider Ownership: 31.5%

Revenue Growth Forecast: 10.8% p.a.

99 Speed Mart Retail Holdings Berhad, a growth company with high insider ownership, has demonstrated strong financial performance. Its revenue is expected to grow 10.8% annually, outpacing the Malaysian market's 6.2%. Earnings grew by 20.4% last year and are forecast to increase by 13.29% per year, surpassing the market's 10.6%. Recent IPO raised MYR 2.36 billion, supporting further expansion. Trading at an attractive valuation below fair value enhances its investment appeal.

- Get an in-depth perspective on 99 Speed Mart Retail Holdings Berhad's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, 99 Speed Mart Retail Holdings Berhad's share price might be too optimistic.

Will Semiconductor (SHSE:603501)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Will Semiconductor Co., Ltd. is a semiconductor design company offering sensor, analog, and touch screen and display solutions with a market cap of CN¥101.72 billion.

Operations: Revenue Segments (in millions of CN¥): Sensor solutions: 5,600; Analog solutions: 3,200; Touch screen and display solutions: 2,400. Will Semiconductor generates revenue from sensor solutions (CN¥5.60 billion), analog solutions (CN¥3.20 billion), and touch screen and display solutions (CN¥2.40 billion).

Insider Ownership: 30.7%

Revenue Growth Forecast: 13.8% p.a.

Will Semiconductor has shown substantial growth, with H1 2024 revenue at CNY 12.09 billion compared to CNY 8.86 billion a year ago, and net income rising to CNY 1.37 billion from CNY 153.12 million. Earnings are forecast to grow significantly at 38.7% annually over the next three years, outpacing the Chinese market's growth rate of 23%. Despite lower future return on equity projections (17.3%), analysts expect a stock price increase of around 46.7%.

- Unlock comprehensive insights into our analysis of Will Semiconductor stock in this growth report.

- The analysis detailed in our Will Semiconductor valuation report hints at an inflated share price compared to its estimated value.

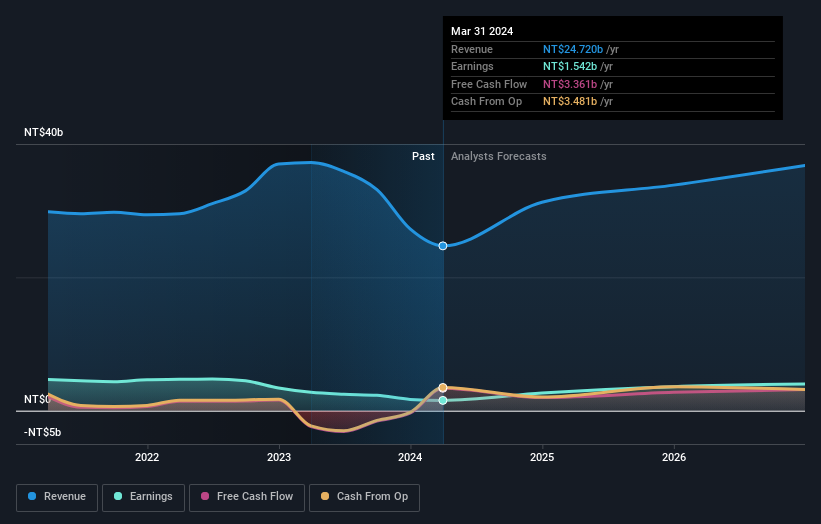

Merida Industry (TWSE:9914)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Merida Industry Co., Ltd. manufactures and sells bicycles and components across Taiwan, China, Hong Kong, Japan, and Europe with a market cap of NT$66.08 billion.

Operations: Revenue from the manufacturing and sales of bicycles and their parts is NT$26.58 billion.

Insider Ownership: 26.8%

Revenue Growth Forecast: 12.7% p.a.

Merida Industry's recent earnings report showed mixed results, with Q2 2024 sales rising to TWD 9.32 billion from TWD 7.46 billion a year ago, but net income slightly declining to TWD 655.55 million from TWD 671.77 million. Despite this, the company's earnings are forecast to grow significantly at 34.6% annually over the next three years, outpacing the Taiwanese market's growth rate of 18.4%. High insider ownership and substantial expected profit growth make it an interesting prospect for investors seeking growth opportunities.

- Take a closer look at Merida Industry's potential here in our earnings growth report.

- The valuation report we've compiled suggests that Merida Industry's current price could be inflated.

Taking Advantage

- Delve into our full catalog of 1504 Fast Growing Companies With High Insider Ownership here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Will Semiconductor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603501

Will Semiconductor

A semiconductor design company, provides sensor solutions, analog solutions and touch screen and display solutions.

Flawless balance sheet with reasonable growth potential.