- China

- /

- Specialty Stores

- /

- SZSE:002780

Beijing Sanfo Outdoor Products Co., Ltd (SZSE:002780) Looks Just Right With A 30% Price Jump

Beijing Sanfo Outdoor Products Co., Ltd (SZSE:002780) shareholders are no doubt pleased to see that the share price has bounced 30% in the last month, although it is still struggling to make up recently lost ground. Taking a wider view, although not as strong as the last month, the full year gain of 14% is also fairly reasonable.

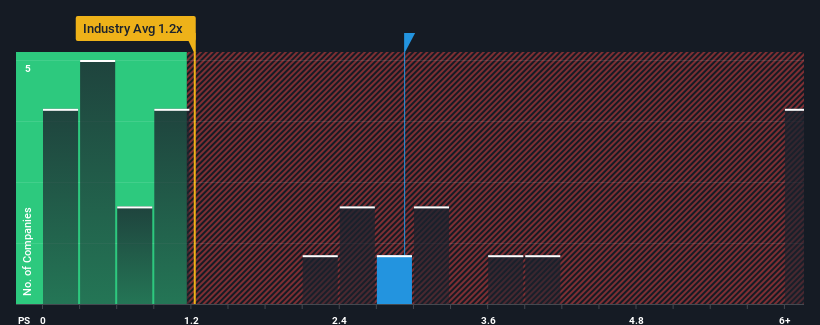

Following the firm bounce in price, when almost half of the companies in China's Specialty Retail industry have price-to-sales ratios (or "P/S") below 1.2x, you may consider Beijing Sanfo Outdoor Products as a stock probably not worth researching with its 2.9x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

View our latest analysis for Beijing Sanfo Outdoor Products

How Has Beijing Sanfo Outdoor Products Performed Recently?

Recent times have been quite advantageous for Beijing Sanfo Outdoor Products as its revenue has been rising very briskly. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Beijing Sanfo Outdoor Products' earnings, revenue and cash flow.How Is Beijing Sanfo Outdoor Products' Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as Beijing Sanfo Outdoor Products' is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company grew revenue by an impressive 30% last year. The strong recent performance means it was also able to grow revenue by 81% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

This is in contrast to the rest of the industry, which is expected to grow by 15% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this information, we can see why Beijing Sanfo Outdoor Products is trading at such a high P/S compared to the industry. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the wider industry.

The Bottom Line On Beijing Sanfo Outdoor Products' P/S

Beijing Sanfo Outdoor Products shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Beijing Sanfo Outdoor Products maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

Before you settle on your opinion, we've discovered 1 warning sign for Beijing Sanfo Outdoor Products that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Sanfo Outdoor Products might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002780

Beijing Sanfo Outdoor Products

Engages in the retail of outdoor sporting goods in China.

Excellent balance sheet and fair value.

Market Insights

Community Narratives