- China

- /

- Real Estate

- /

- SZSE:000002

Why Investors Shouldn't Be Surprised By China Vanke Co., Ltd.'s (SZSE:000002) 25% Share Price Plunge

The China Vanke Co., Ltd. (SZSE:000002) share price has fared very poorly over the last month, falling by a substantial 25%. For any long-term shareholders, the last month ends a year to forget by locking in a 56% share price decline.

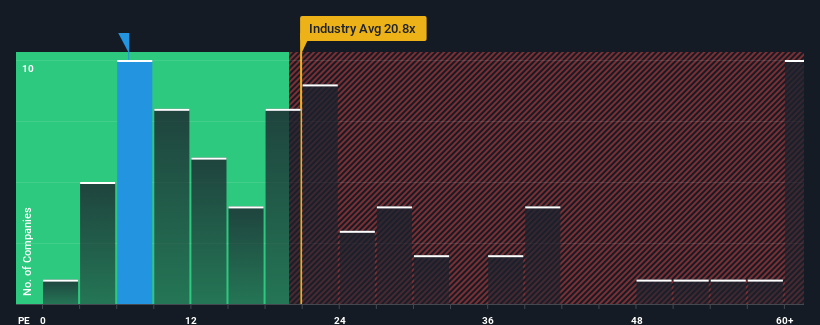

Since its price has dipped substantially, China Vanke may be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 6.9x, since almost half of all companies in China have P/E ratios greater than 30x and even P/E's higher than 54x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

While the market has experienced earnings growth lately, China Vanke's earnings have gone into reverse gear, which is not great. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

View our latest analysis for China Vanke

Is There Any Growth For China Vanke?

There's an inherent assumption that a company should far underperform the market for P/E ratios like China Vanke's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 47%. The last three years don't look nice either as the company has shrunk EPS by 72% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings growth is heading into negative territory, declining 4.7% per year over the next three years. With the market predicted to deliver 21% growth each year, that's a disappointing outcome.

With this information, we are not surprised that China Vanke is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Final Word

Shares in China Vanke have plummeted and its P/E is now low enough to touch the ground. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that China Vanke maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

There are also other vital risk factors to consider and we've discovered 2 warning signs for China Vanke (1 is potentially serious!) that you should be aware of before investing here.

If you're unsure about the strength of China Vanke's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000002

China Vanke

Engages in the development and sale of properties in the Mainland China, Hong Kong, and internationally.

Good value with moderate growth potential.

Market Insights

Community Narratives