Subdued Growth No Barrier To Zhejiang Garden Biopharmaceutical Co.,Ltd. (SZSE:300401) With Shares Advancing 27%

Despite an already strong run, Zhejiang Garden Biopharmaceutical Co.,Ltd. (SZSE:300401) shares have been powering on, with a gain of 27% in the last thirty days. Notwithstanding the latest gain, the annual share price return of 4.5% isn't as impressive.

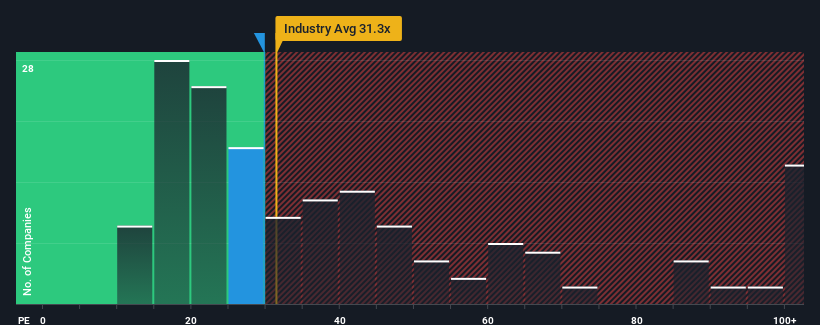

In spite of the firm bounce in price, there still wouldn't be many who think Zhejiang Garden BiopharmaceuticalLtd's price-to-earnings (or "P/E") ratio of 29.8x is worth a mention when the median P/E in China is similar at about 32x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

As an illustration, earnings have deteriorated at Zhejiang Garden BiopharmaceuticalLtd over the last year, which is not ideal at all. It might be that many expect the company to put the disappointing earnings performance behind them over the coming period, which has kept the P/E from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

View our latest analysis for Zhejiang Garden BiopharmaceuticalLtd

Is There Some Growth For Zhejiang Garden BiopharmaceuticalLtd?

There's an inherent assumption that a company should be matching the market for P/E ratios like Zhejiang Garden BiopharmaceuticalLtd's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 16%. This means it has also seen a slide in earnings over the longer-term as EPS is down 23% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Comparing that to the market, which is predicted to deliver 39% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

With this information, we find it concerning that Zhejiang Garden BiopharmaceuticalLtd is trading at a fairly similar P/E to the market. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Key Takeaway

Zhejiang Garden BiopharmaceuticalLtd appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Zhejiang Garden BiopharmaceuticalLtd revealed its shrinking earnings over the medium-term aren't impacting its P/E as much as we would have predicted, given the market is set to grow. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless the recent medium-term conditions improve, it's challenging to accept these prices as being reasonable.

Having said that, be aware Zhejiang Garden BiopharmaceuticalLtd is showing 2 warning signs in our investment analysis, and 1 of those is concerning.

If you're unsure about the strength of Zhejiang Garden BiopharmaceuticalLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Garden BiopharmaceuticalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300401

Zhejiang Garden BiopharmaceuticalLtd

Zhejiang Garden Biopharmaceutical Co.,Ltd.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives