Advertisement

Is Yantai Dongcheng Pharmaceutical GroupLtd (SZSE:002675) A Risky Investment?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Yantai Dongcheng Pharmaceutical Group Co.,Ltd. (SZSE:002675) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Yantai Dongcheng Pharmaceutical GroupLtd

What Is Yantai Dongcheng Pharmaceutical GroupLtd's Net Debt?

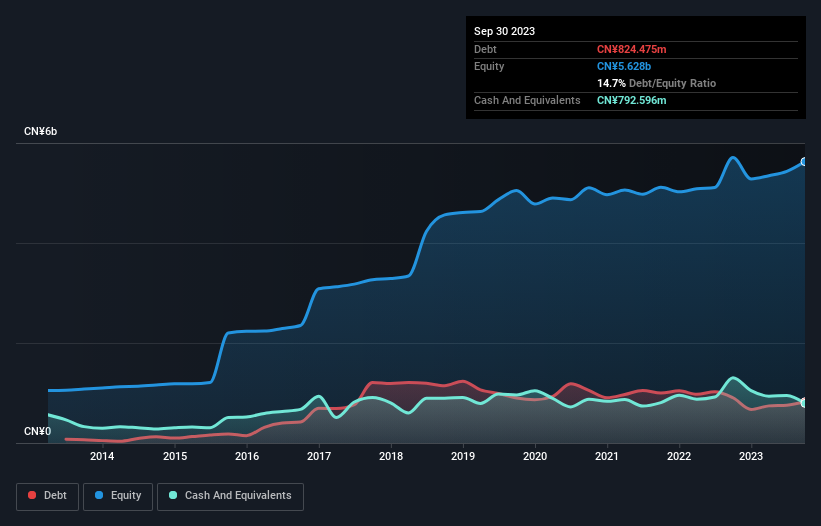

The image below, which you can click on for greater detail, shows that Yantai Dongcheng Pharmaceutical GroupLtd had debt of CN¥824.5m at the end of September 2023, a reduction from CN¥905.1m over a year. On the flip side, it has CN¥792.6m in cash leading to net debt of about CN¥31.9m.

How Strong Is Yantai Dongcheng Pharmaceutical GroupLtd's Balance Sheet?

The latest balance sheet data shows that Yantai Dongcheng Pharmaceutical GroupLtd had liabilities of CN¥2.12b due within a year, and liabilities of CN¥544.0m falling due after that. Offsetting these obligations, it had cash of CN¥792.6m as well as receivables valued at CN¥835.1m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥1.03b.

Given Yantai Dongcheng Pharmaceutical GroupLtd has a market capitalization of CN¥13.0b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Carrying virtually no net debt, Yantai Dongcheng Pharmaceutical GroupLtd has a very light debt load indeed.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Yantai Dongcheng Pharmaceutical GroupLtd has very little debt (net of cash), and boasts a debt to EBITDA ratio of 0.053 and EBIT of 16.4 times the interest expense. Indeed relative to its earnings its debt load seems light as a feather. It is just as well that Yantai Dongcheng Pharmaceutical GroupLtd's load is not too heavy, because its EBIT was down 21% over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Yantai Dongcheng Pharmaceutical GroupLtd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Yantai Dongcheng Pharmaceutical GroupLtd recorded free cash flow worth 54% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Yantai Dongcheng Pharmaceutical GroupLtd's EBIT growth rate was a real negative on this analysis, although the other factors we considered were considerably better. There's no doubt that its ability to to cover its interest expense with its EBIT is pretty flash. Considering this range of data points, we think Yantai Dongcheng Pharmaceutical GroupLtd is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 1 warning sign for Yantai Dongcheng Pharmaceutical GroupLtd that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002675

Yantai Dongcheng Pharmaceutical GroupLtd

Engages in the manufacture and sale of biochemical APIs, finished dosage forms, nuclide drugs, and healthy products for cardiovascular, antitumor, urology, orthopedics, and other therapeutic areas.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor