Advertisement

Shenzhen Hepalink Pharmaceutical Group Co., Ltd.'s (SZSE:002399) Business Is Trailing The Industry But Its Shares Aren't

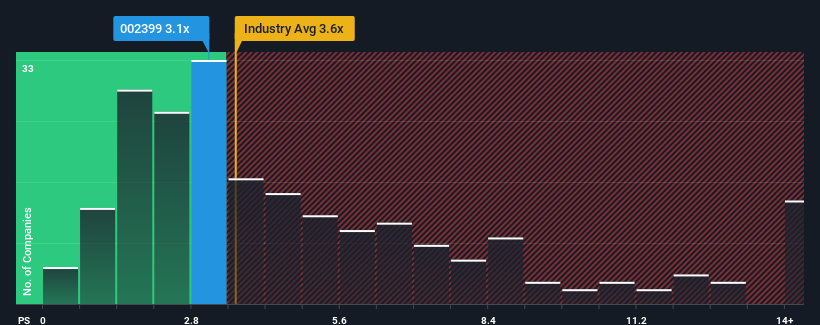

It's not a stretch to say that Shenzhen Hepalink Pharmaceutical Group Co., Ltd.'s (SZSE:002399) price-to-sales (or "P/S") ratio of 3.1x right now seems quite "middle-of-the-road" for companies in the Pharmaceuticals industry in China, where the median P/S ratio is around 3.6x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Shenzhen Hepalink Pharmaceutical Group

How Shenzhen Hepalink Pharmaceutical Group Has Been Performing

While the industry has experienced revenue growth lately, Shenzhen Hepalink Pharmaceutical Group's revenue has gone into reverse gear, which is not great. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Shenzhen Hepalink Pharmaceutical Group.How Is Shenzhen Hepalink Pharmaceutical Group's Revenue Growth Trending?

In order to justify its P/S ratio, Shenzhen Hepalink Pharmaceutical Group would need to produce growth that's similar to the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 6.5%. The last three years don't look nice either as the company has shrunk revenue by 15% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 1.3% as estimated by the one analyst watching the company. With the industry predicted to deliver 207% growth, the company is positioned for a weaker revenue result.

With this in mind, we find it intriguing that Shenzhen Hepalink Pharmaceutical Group's P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What We Can Learn From Shenzhen Hepalink Pharmaceutical Group's P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Given that Shenzhen Hepalink Pharmaceutical Group's revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Shenzhen Hepalink Pharmaceutical Group with six simple checks will allow you to discover any risks that could be an issue.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002399

Shenzhen Hepalink Pharmaceutical Group

Shenzhen Hepalink Pharmaceutical Group Co., Ltd.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor