Advertisement

Does Zhejiang Hisoar Pharmaceutical (SZSE:002099) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Zhejiang Hisoar Pharmaceutical Co., Ltd. (SZSE:002099) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Zhejiang Hisoar Pharmaceutical

What Is Zhejiang Hisoar Pharmaceutical's Debt?

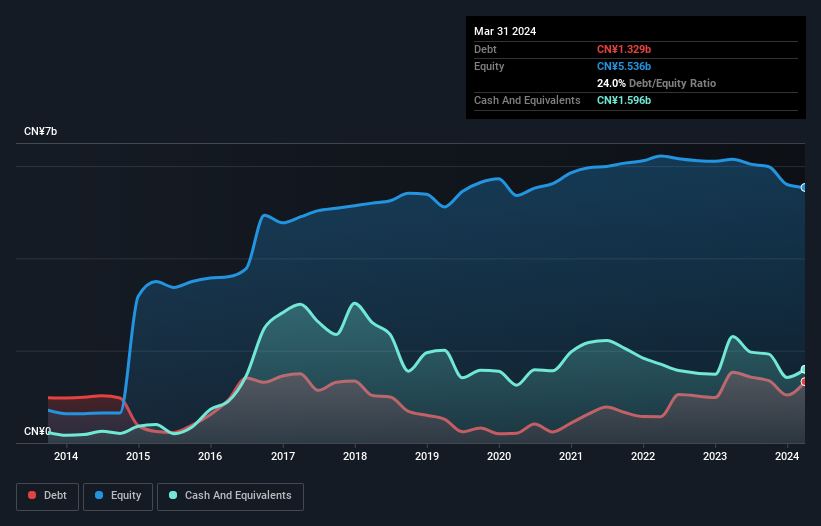

As you can see below, Zhejiang Hisoar Pharmaceutical had CN¥1.33b of debt at March 2024, down from CN¥1.53b a year prior. But it also has CN¥1.60b in cash to offset that, meaning it has CN¥266.9m net cash.

How Strong Is Zhejiang Hisoar Pharmaceutical's Balance Sheet?

The latest balance sheet data shows that Zhejiang Hisoar Pharmaceutical had liabilities of CN¥1.90b due within a year, and liabilities of CN¥216.9m falling due after that. Offsetting this, it had CN¥1.60b in cash and CN¥514.7m in receivables that were due within 12 months. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that Zhejiang Hisoar Pharmaceutical's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the CN¥8.67b company is struggling for cash, we still think it's worth monitoring its balance sheet. Despite its noteworthy liabilities, Zhejiang Hisoar Pharmaceutical boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is Zhejiang Hisoar Pharmaceutical's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Zhejiang Hisoar Pharmaceutical had a loss before interest and tax, and actually shrunk its revenue by 18%, to CN¥2.1b. We would much prefer see growth.

So How Risky Is Zhejiang Hisoar Pharmaceutical?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Zhejiang Hisoar Pharmaceutical had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through CN¥33m of cash and made a loss of CN¥430m. Given it only has net cash of CN¥266.9m, the company may need to raise more capital if it doesn't reach break-even soon. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Zhejiang Hisoar Pharmaceutical has 1 warning sign we think you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Hisoar Pharmaceutical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002099

Zhejiang Hisoar Pharmaceutical

Engages in the manufacture of pharmaceutical products and dyes in China and internationally.

Mediocre balance sheet and overvalued.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor