November 2024's Leading Growth Companies With Significant Insider Ownership

Reviewed by Simply Wall St

As global markets experience broad-based gains, with U.S. indexes nearing record highs and smaller-cap indexes outperforming large-caps, investors are closely watching economic indicators such as jobless claims and home sales that suggest continued economic growth. In this environment of cautious optimism, growth companies with significant insider ownership can be particularly appealing, as high insider stakes may indicate confidence in the company's long-term potential amidst the current market dynamics.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 32.4% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.9% | 37.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.6% |

| Pharma Mar (BME:PHM) | 11.8% | 56.9% |

| Findi (ASX:FND) | 34.8% | 71.5% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 103.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| Alkami Technology (NasdaqGS:ALKT) | 11% | 98.6% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.7% | 95% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

We're going to check out a few of the best picks from our screener tool.

Beijing Konruns PharmaceuticalLtd (SHSE:603590)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beijing Konruns Pharmaceutical Co., Ltd. is involved in the research, development, production, and sale of pharmaceuticals both in China and internationally, with a market cap of CN¥3.99 billion.

Operations: The company's revenue is primarily derived from its Pharmaceutical Manufacturing segment, which generated CN¥846.29 million.

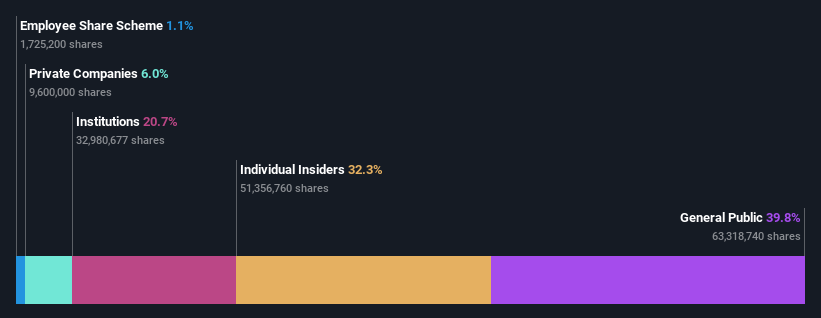

Insider Ownership: 32.3%

Earnings Growth Forecast: 34.3% p.a.

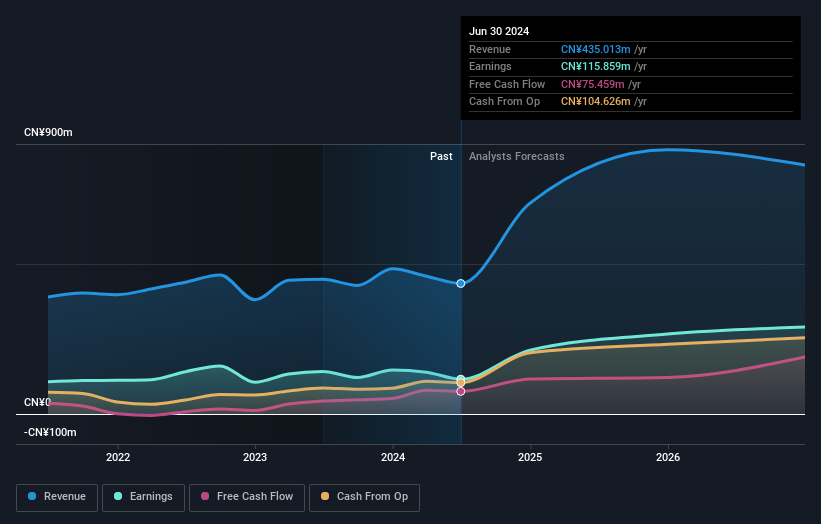

Beijing Konruns Pharmaceutical demonstrates potential as a growth company with expected annual earnings growth of 34.3%, surpassing the CN market's 26.2%. Despite this, recent financial results show challenges, with nine-month revenue declining to CNY 646.31 million from CNY 720.04 million and net income dropping to CNY 112.98 million from CNY 148.63 million year-over-year. The company's price-to-earnings ratio of 34.9x remains competitive within the market context at 35.4x, suggesting reasonable valuation amidst its growth trajectory.

- Delve into the full analysis future growth report here for a deeper understanding of Beijing Konruns PharmaceuticalLtd.

- In light of our recent valuation report, it seems possible that Beijing Konruns PharmaceuticalLtd is trading beyond its estimated value.

Shanghai Luoman Technologies (SHSE:605289)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Luoman Lighting Technologies Inc. operates in the lighting technology sector and has a market capitalization of CN¥2.61 billion.

Operations: Shanghai Luoman Technologies generates its revenue from various segments within the lighting technology industry.

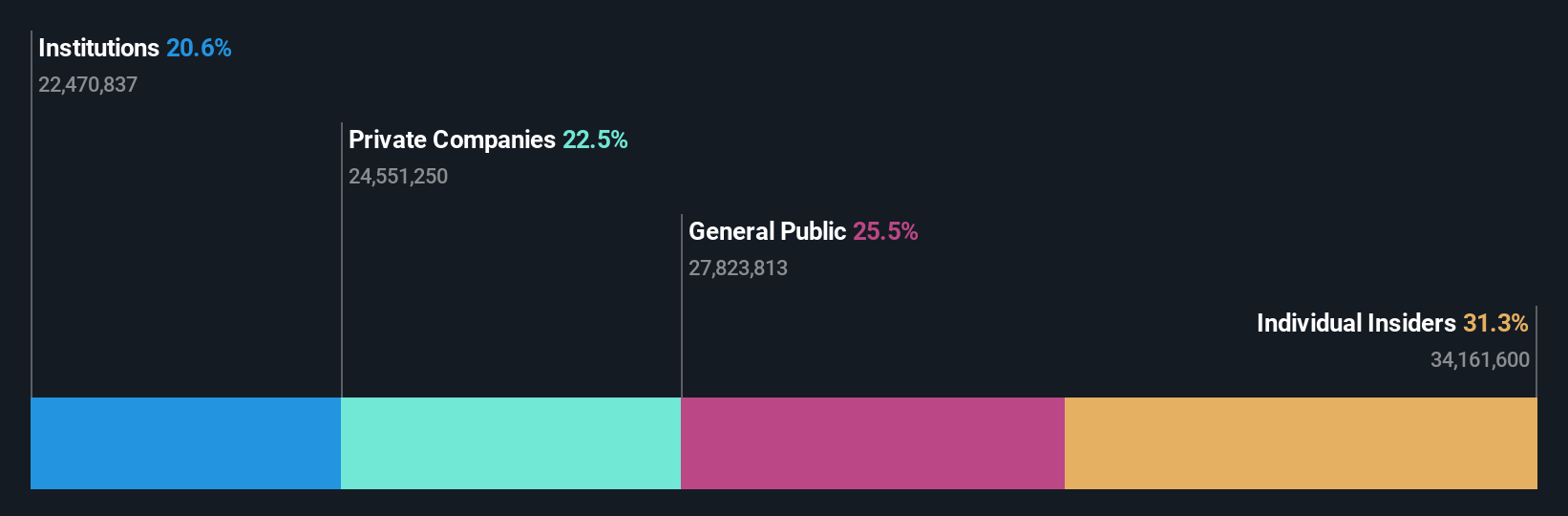

Insider Ownership: 29.8%

Earnings Growth Forecast: 49.8% p.a.

Shanghai Luoman Technologies faces mixed prospects with earnings expected to grow significantly at 49.8% annually, outpacing the CN market's 26.2%. Despite this growth potential, recent results show a decline in net income to CNY 15.79 million from CNY 75.54 million year-over-year, impacting profit margins and earnings per share. Revenue increased to CNY 448.89 million from CNY 405.13 million, indicating positive sales momentum amidst challenges in profitability and dividend sustainability at a rate of 1.02%.

- Click to explore a detailed breakdown of our findings in Shanghai Luoman Technologies' earnings growth report.

- According our valuation report, there's an indication that Shanghai Luoman Technologies' share price might be on the expensive side.

Chison Medical Technologies (SHSE:688358)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chison Medical Technologies Co., Ltd. manufactures and sells diagnostic ultrasound systems both in China and internationally, with a market cap of CN¥2.99 billion.

Operations: The company generates revenue of CN¥444.28 million from its Ultrasound Medical Imaging Equipment Business.

Insider Ownership: 23.6%

Earnings Growth Forecast: 34.9% p.a.

Chison Medical Technologies shows potential with earnings forecasted to grow significantly at 34.9% annually, surpassing the CN market's 26.2%. However, recent results indicate a decline in net income to CNY 98.41 million from CNY 141.43 million year-over-year, affecting profitability and earnings per share. Despite trading at a substantial discount below its estimated fair value and expected revenue growth of 25.1% annually, dividend sustainability remains a concern with coverage challenges from free cash flows.

- Click here to discover the nuances of Chison Medical Technologies with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Chison Medical Technologies is trading behind its estimated value.

Make It Happen

- Discover the full array of 1516 Fast Growing Companies With High Insider Ownership right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Konruns PharmaceuticalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603590

Beijing Konruns PharmaceuticalLtd

Engages in the research and development, production, and sale of pharmaceuticals in China and internationally.

High growth potential with excellent balance sheet.