Advertisement

Subdued Growth No Barrier To Zhejiang Shengda Bio-Pharm Co., Ltd. (SHSE:603079) With Shares Advancing 28%

The Zhejiang Shengda Bio-Pharm Co., Ltd. (SHSE:603079) share price has done very well over the last month, posting an excellent gain of 28%. Unfortunately, despite the strong performance over the last month, the full year gain of 7.8% isn't as attractive.

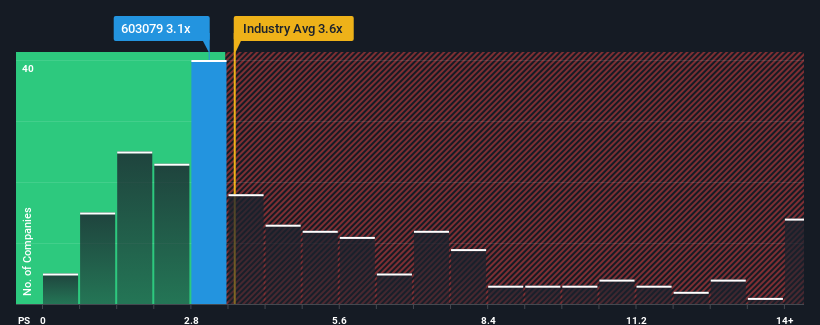

Although its price has surged higher, there still wouldn't be many who think Zhejiang Shengda Bio-Pharm's price-to-sales (or "P/S") ratio of 3.1x is worth a mention when the median P/S in China's Pharmaceuticals industry is similar at about 3.6x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Zhejiang Shengda Bio-Pharm

How Zhejiang Shengda Bio-Pharm Has Been Performing

Zhejiang Shengda Bio-Pharm has been doing a decent job lately as it's been growing revenue at a reasonable pace. It might be that many expect the respectable revenue performance to only match most other companies over the coming period, which has kept the P/S from rising. If not, then at least existing shareholders probably aren't too pessimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Zhejiang Shengda Bio-Pharm will help you shine a light on its historical performance.How Is Zhejiang Shengda Bio-Pharm's Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Zhejiang Shengda Bio-Pharm's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 6.2%. Although, the latest three year period in total hasn't been as good as it didn't manage to provide any growth at all. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Comparing that to the industry, which is predicted to deliver 237% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this information, we find it interesting that Zhejiang Shengda Bio-Pharm is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

The Bottom Line On Zhejiang Shengda Bio-Pharm's P/S

Zhejiang Shengda Bio-Pharm appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Zhejiang Shengda Bio-Pharm revealed its poor three-year revenue trends aren't resulting in a lower P/S as per our expectations, given they look worse than current industry outlook. When we see weak revenue with slower than industry growth, we suspect the share price is at risk of declining, bringing the P/S back in line with expectations. If recent medium-term revenue trends continue, the probability of a share price decline will become quite substantial, placing shareholders at risk.

Before you take the next step, you should know about the 1 warning sign for Zhejiang Shengda Bio-Pharm that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Shengda Bio-Pharm might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603079

Zhejiang Shengda Bio-Pharm

Develops, produces, and sells food and feed additives for pharmaceutical, nutritional, food, and animal feed industry.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor