Jiangsu Kanion Pharmaceutical Co.,Ltd.'s (SHSE:600557) Share Price Boosted 34% But Its Business Prospects Need A Lift Too

Jiangsu Kanion Pharmaceutical Co.,Ltd. (SHSE:600557) shares have had a really impressive month, gaining 34% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 27% in the last twelve months.

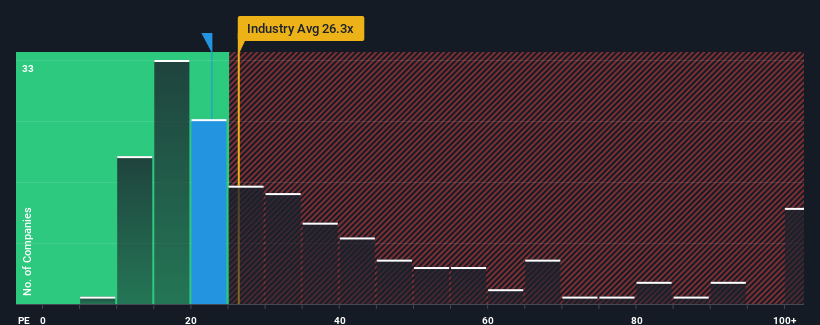

Even after such a large jump in price, Jiangsu Kanion PharmaceuticalLtd may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 22.7x, since almost half of all companies in China have P/E ratios greater than 31x and even P/E's higher than 56x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Jiangsu Kanion PharmaceuticalLtd certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Jiangsu Kanion PharmaceuticalLtd

Does Growth Match The Low P/E?

Jiangsu Kanion PharmaceuticalLtd's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 26%. Pleasingly, EPS has also lifted 53% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 20% during the coming year according to the eight analysts following the company. With the market predicted to deliver 42% growth , the company is positioned for a weaker earnings result.

In light of this, it's understandable that Jiangsu Kanion PharmaceuticalLtd's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Jiangsu Kanion PharmaceuticalLtd's P/E?

Despite Jiangsu Kanion PharmaceuticalLtd's shares building up a head of steam, its P/E still lags most other companies. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Jiangsu Kanion PharmaceuticalLtd maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Plus, you should also learn about this 1 warning sign we've spotted with Jiangsu Kanion PharmaceuticalLtd.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600557

Jiangsu Kanion PharmaceuticalLtd

Researches and develops, produces, and sells Chinese medicines.

Flawless balance sheet with reasonable growth potential.

Market Insights

Community Narratives