Advertisement

- China

- /

- Entertainment

- /

- SZSE:300860

There May Be Underlying Issues With The Quality Of Funshine Culture GroupLtd's (SZSE:300860) Earnings

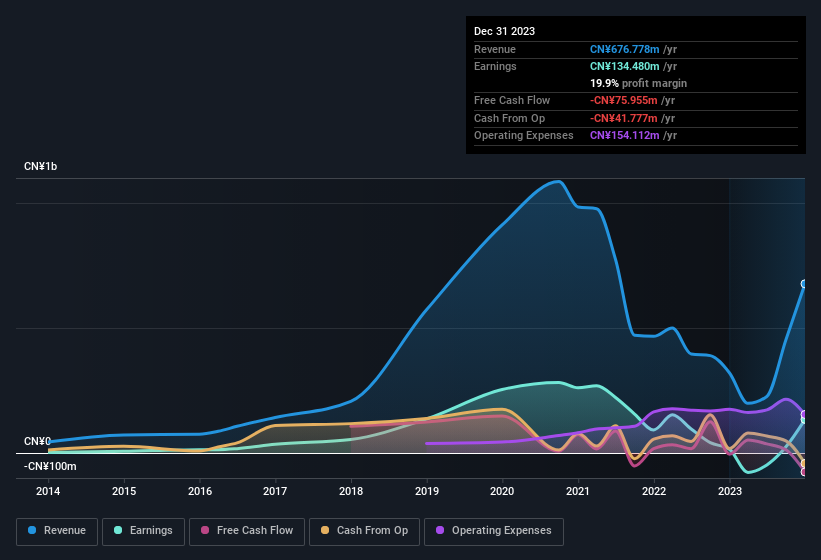

Despite posting some strong earnings, the market for Funshine Culture Group Co.,Ltd.'s (SZSE:300860) stock hasn't moved much. We did some digging, and we found some concerning factors in the details.

See our latest analysis for Funshine Culture GroupLtd

Zooming In On Funshine Culture GroupLtd's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to December 2023, Funshine Culture GroupLtd had an accrual ratio of 0.74. As a general rule, that bodes poorly for future profitability. And indeed, during the period the company didn't produce any free cash flow whatsoever. Even though it reported a profit of CN¥134.5m, a look at free cash flow indicates it actually burnt through CN¥76m in the last year. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of CN¥76m, this year, indicates high risk.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Funshine Culture GroupLtd's Profit Performance

As we discussed above, we think Funshine Culture GroupLtd's earnings were not supported by free cash flow, which might concern some investors. As a result, we think it may well be the case that Funshine Culture GroupLtd's underlying earnings power is lower than its statutory profit. But the happy news is that, while acknowledging we have to look beyond the statutory numbers, those numbers are still improving, with EPS growing at a very high rate over the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. For example, Funshine Culture GroupLtd has 3 warning signs (and 1 which is potentially serious) we think you should know about.

Today we've zoomed in on a single data point to better understand the nature of Funshine Culture GroupLtd's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300860

Funshine Culture GroupLtd

Engages in cultural performing events, cultural tourism, and public artistic lighting business in China.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor