- China

- /

- Entertainment

- /

- SZSE:300315

Optimistic Investors Push Ourpalm Co., Ltd. (SZSE:300315) Shares Up 34% But Growth Is Lacking

The Ourpalm Co., Ltd. (SZSE:300315) share price has done very well over the last month, posting an excellent gain of 34%. Taking a wider view, although not as strong as the last month, the full year gain of 15% is also fairly reasonable.

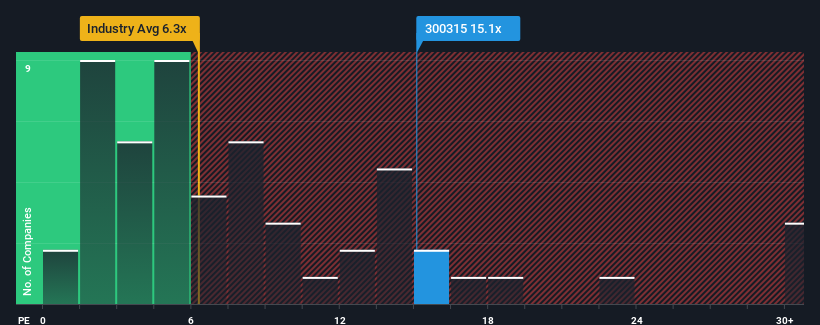

After such a large jump in price, Ourpalm may be sending strong sell signals at present with a price-to-sales (or "P/S") ratio of 15.1x, when you consider almost half of the companies in the Entertainment industry in China have P/S ratios under 6.3x and even P/S lower than 3x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for Ourpalm

How Ourpalm Has Been Performing

Ourpalm could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It might be that many expect the dour revenue performance to recover substantially, which has kept the P/S from collapsing. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Ourpalm will help you uncover what's on the horizon.How Is Ourpalm's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as Ourpalm's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 3.1%. The last three years don't look nice either as the company has shrunk revenue by 41% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 6.9% during the coming year according to the only analyst following the company. Meanwhile, the rest of the industry is forecast to expand by 28%, which is noticeably more attractive.

With this information, we find it concerning that Ourpalm is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Bottom Line On Ourpalm's P/S

The strong share price surge has lead to Ourpalm's P/S soaring as well. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

It comes as a surprise to see Ourpalm trade at such a high P/S given the revenue forecasts look less than stellar. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. At these price levels, investors should remain cautious, particularly if things don't improve.

Having said that, be aware Ourpalm is showing 1 warning sign in our investment analysis, you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300315

Ourpalm

Focuses on the development, distribution, and operation of online games in China and internationally.

Excellent balance sheet very low.

Similar Companies

Market Insights

Community Narratives