Advertisement

Revenues Not Telling The Story For Tangel Culture Co., Ltd. (SZSE:300148) After Shares Rise 27%

Those holding Tangel Culture Co., Ltd. (SZSE:300148) shares would be relieved that the share price has rebounded 27% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 12% in the last twelve months.

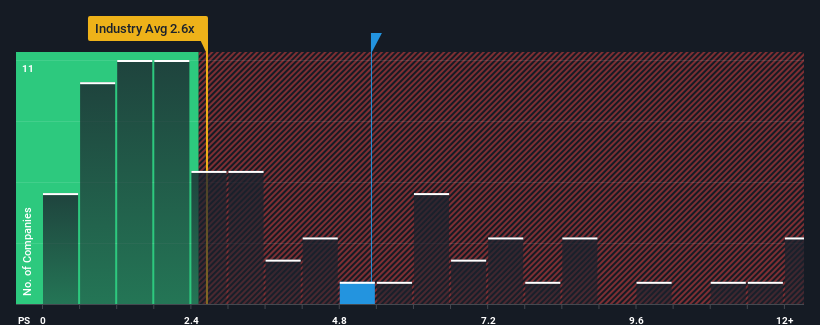

After such a large jump in price, given around half the companies in China's Media industry have price-to-sales ratios (or "P/S") below 2.6x, you may consider Tangel Culture as a stock to avoid entirely with its 5.3x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Tangel Culture

What Does Tangel Culture's Recent Performance Look Like?

As an illustration, revenue has deteriorated at Tangel Culture over the last year, which is not ideal at all. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. If not, then existing shareholders may be quite nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Tangel Culture's earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Tangel Culture's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 2.9% decrease to the company's top line. As a result, revenue from three years ago have also fallen 52% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 20% shows it's an unpleasant look.

In light of this, it's alarming that Tangel Culture's P/S sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Final Word

The strong share price surge has lead to Tangel Culture's P/S soaring as well. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Tangel Culture revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Tangel Culture with six simple checks.

If these risks are making you reconsider your opinion on Tangel Culture, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Tangel Culture might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300148

Tangel Culture

Engages in the research and development, distribution, agency, and operation of mobile games, book publishing and distribution, and educational businesses in China.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor