- China

- /

- Entertainment

- /

- SHSE:603258

Why Investors Shouldn't Be Surprised By Hangzhou Electronic Soul Network Technology Co., Ltd.'s (SHSE:603258) 29% Share Price Surge

Hangzhou Electronic Soul Network Technology Co., Ltd. (SHSE:603258) shareholders are no doubt pleased to see that the share price has bounced 29% in the last month, although it is still struggling to make up recently lost ground. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 20% in the last twelve months.

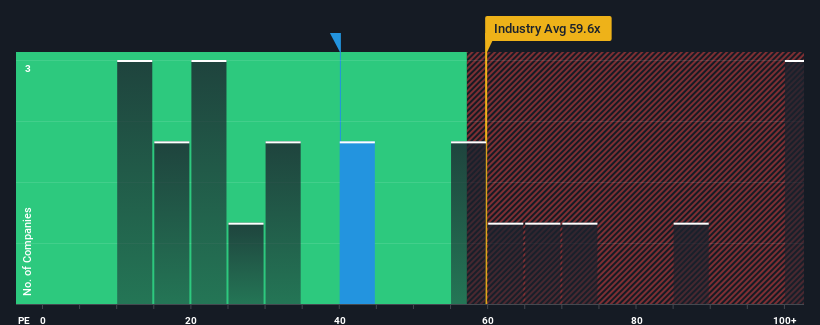

After such a large jump in price, given around half the companies in China have price-to-earnings ratios (or "P/E's") below 29x, you may consider Hangzhou Electronic Soul Network Technology as a stock to potentially avoid with its 40x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Hangzhou Electronic Soul Network Technology has been struggling lately as its earnings have declined faster than most other companies. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. If not, then existing shareholders may be very nervous about the viability of the share price.

View our latest analysis for Hangzhou Electronic Soul Network Technology

How Is Hangzhou Electronic Soul Network Technology's Growth Trending?

In order to justify its P/E ratio, Hangzhou Electronic Soul Network Technology would need to produce impressive growth in excess of the market.

Retrospectively, the last year delivered a frustrating 52% decrease to the company's bottom line. As a result, earnings from three years ago have also fallen 70% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 187% as estimated by the sole analyst watching the company. With the market only predicted to deliver 41%, the company is positioned for a stronger earnings result.

With this information, we can see why Hangzhou Electronic Soul Network Technology is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Hangzhou Electronic Soul Network Technology's P/E?

Hangzhou Electronic Soul Network Technology's P/E is getting right up there since its shares have risen strongly. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Hangzhou Electronic Soul Network Technology's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

It is also worth noting that we have found 3 warning signs for Hangzhou Electronic Soul Network Technology (1 is potentially serious!) that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

If you're looking to trade Hangzhou Electronic Soul Network Technology, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hangzhou Electronic Soul Network Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603258

Hangzhou Electronic Soul Network Technology

Develops and publishes online and mobile games in China and internationally.

Flawless balance sheet and overvalued.

Market Insights

Community Narratives