- China

- /

- Metals and Mining

- /

- SZSE:301307

Investors Appear Satisfied With Chongqing Millison Technologies INC.'s (SZSE:301307) Prospects As Shares Rocket 32%

Chongqing Millison Technologies INC. (SZSE:301307) shares have continued their recent momentum with a 32% gain in the last month alone. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 17% over that time.

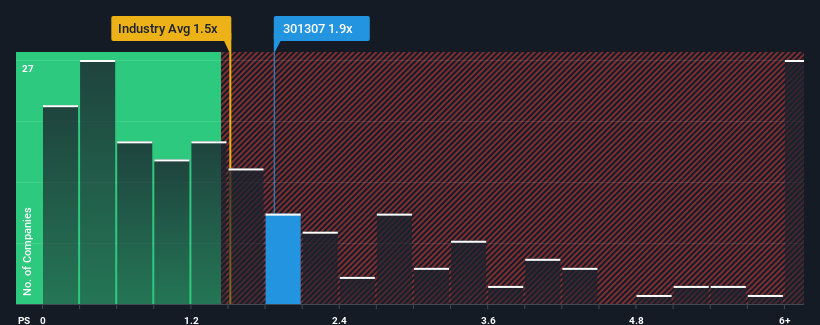

Although its price has surged higher, there still wouldn't be many who think Chongqing Millison Technologies' price-to-sales (or "P/S") ratio of 1.9x is worth a mention when the median P/S in China's Metals and Mining industry is similar at about 1.5x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Chongqing Millison Technologies

What Does Chongqing Millison Technologies' Recent Performance Look Like?

The recent revenue growth at Chongqing Millison Technologies would have to be considered satisfactory if not spectacular. One possibility is that the P/S is moderate because investors think this good revenue growth might only be parallel to the broader industry in the near future. Those who are bullish on Chongqing Millison Technologies will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Chongqing Millison Technologies will help you shine a light on its historical performance.How Is Chongqing Millison Technologies' Revenue Growth Trending?

In order to justify its P/S ratio, Chongqing Millison Technologies would need to produce growth that's similar to the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.3% last year. The latest three year period has also seen an excellent 50% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Weighing that recent medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 15% shows it's about the same on an annualised basis.

With this information, we can see why Chongqing Millison Technologies is trading at a fairly similar P/S to the industry. It seems most investors are expecting to see average growth rates continue into the future and are only willing to pay a moderate amount for the stock.

The Key Takeaway

Its shares have lifted substantially and now Chongqing Millison Technologies' P/S is back within range of the industry median. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

It appears to us that Chongqing Millison Technologies maintains its moderate P/S off the back of its recent three-year growth being in line with the wider industry forecast. With previous revenue trends that keep up with the current industry outlook, it's hard to justify the company's P/S ratio deviating much from it's current point. Unless the recent medium-term conditions change, they will continue to support the share price at these levels.

You should always think about risks. Case in point, we've spotted 1 warning sign for Chongqing Millison Technologies you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

If you're looking to trade Chongqing Millison Technologies, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301307

Chongqing Millison Technologies

Engages in the research, development, production, and sale of aluminum alloy precision die castings for the communication and automotive sectors in China.

Excellent balance sheet and slightly overvalued.