- China

- /

- Metals and Mining

- /

- SZSE:301261

Why Investors Shouldn't Be Surprised By Hengong Precision Equipment Co., Ltd.'s (SZSE:301261) 39% Share Price Surge

Despite an already strong run, Hengong Precision Equipment Co., Ltd. (SZSE:301261) shares have been powering on, with a gain of 39% in the last thirty days. The last 30 days bring the annual gain to a very sharp 93%.

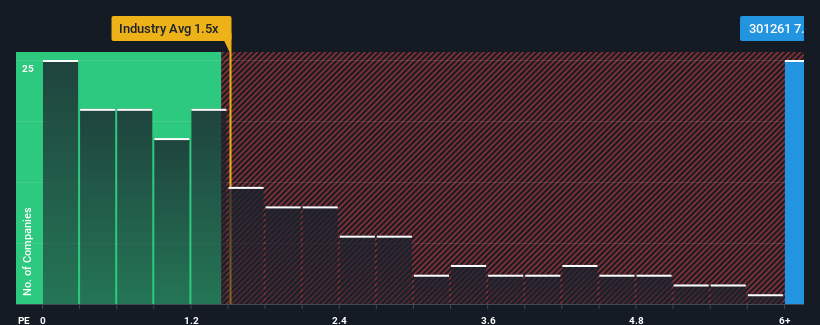

After such a large jump in price, given around half the companies in China's Metals and Mining industry have price-to-sales ratios (or "P/S") below 1.5x, you may consider Hengong Precision Equipment as a stock to avoid entirely with its 7.8x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Hengong Precision Equipment

What Does Hengong Precision Equipment's P/S Mean For Shareholders?

Recent times have been advantageous for Hengong Precision Equipment as its revenues have been rising faster than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Hengong Precision Equipment's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as steep as Hengong Precision Equipment's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, we see that the company grew revenue by an impressive 17% last year. The latest three year period has also seen a 18% overall rise in revenue, aided extensively by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 35% as estimated by the sole analyst watching the company. With the industry only predicted to deliver 14%, the company is positioned for a stronger revenue result.

With this information, we can see why Hengong Precision Equipment is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Hengong Precision Equipment's P/S

Shares in Hengong Precision Equipment have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look into Hengong Precision Equipment shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Before you take the next step, you should know about the 2 warning signs for Hengong Precision Equipment (1 can't be ignored!) that we have uncovered.

If these risks are making you reconsider your opinion on Hengong Precision Equipment, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade Hengong Precision Equipment, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hengong Precision Equipment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301261

Hengong Precision Equipment

Engages in the research and development, production and processing, and sales services of new fluid technology materials in China and internationally.

High growth potential with adequate balance sheet.

Market Insights

Community Narratives