Amidst a backdrop of economic uncertainty and inflation concerns, global markets have been grappling with trade policy shifts and fluctuating consumer sentiment. As investors navigate these turbulent waters, companies with high insider ownership often attract attention due to the confidence insiders demonstrate in their business prospects. In this context, growth companies where insiders hold significant stakes can offer intriguing opportunities for those seeking alignment between management and shareholder interests.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 24.7% |

| Pharma Mar (BME:PHM) | 11.8% | 40.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 47.2% |

| Vow (OB:VOW) | 13.1% | 111.2% |

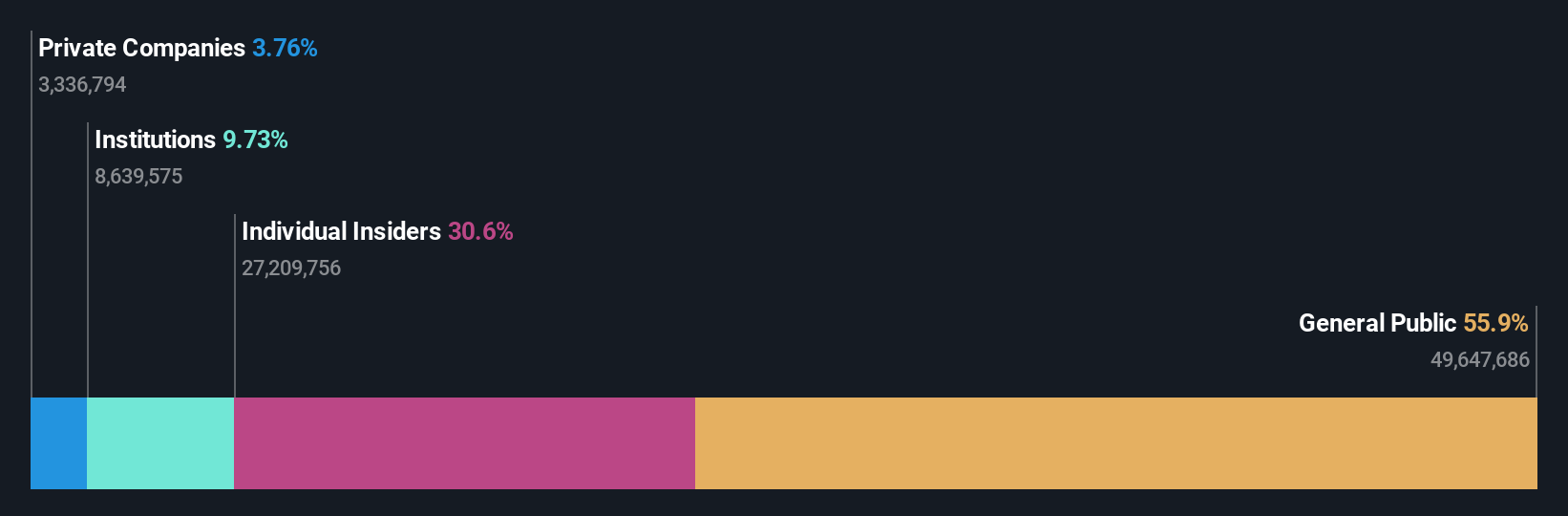

| Global Tax Free (KOSDAQ:A204620) | 21.8% | 35.1% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| CD Projekt (WSE:CDR) | 29.7% | 36.8% |

| Nordic Halibut (OB:NOHAL) | 29.8% | 56.3% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 83.6% |

Let's take a closer look at a couple of our picks from the screened companies.

ALTEOGEN (KOSDAQ:A196170)

Simply Wall St Growth Rating: ★★★★★★

Overview: ALTEOGEN Inc. is a biotechnology company that specializes in developing long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars with a market cap of ₩18.97 trillion.

Operations: ALTEOGEN Inc. generates revenue primarily through its development of long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars.

Insider Ownership: 25.9%

ALTEOGEN's earnings are forecast to grow significantly at 96.3% annually, outpacing the KR market. The company's revenue is also expected to rise rapidly by 74.4% per year, well above the market average of 8%. Recently, ALTEOGEN completed a private placement totaling approximately KRW 155 billion in preferred stock, indicating strong institutional interest and potential for growth. Despite trading below estimated fair value, no substantial insider trading activity has been noted recently.

- Click to explore a detailed breakdown of our findings in ALTEOGEN's earnings growth report.

- The valuation report we've compiled suggests that ALTEOGEN's current price could be inflated.

Beijing Hotgen Biotech (SHSE:688068)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beijing Hotgen Biotech Co., Ltd. specializes in the research, development, manufacture, and sale of in-vitro diagnostic products for medical and public safety inspection within the biomedicine field, with a market cap of CN¥8.56 billion.

Operations: The company generates revenue of CN¥510.89 million from its medical labs and research segment.

Insider Ownership: 31.8%

Beijing Hotgen Biotech is positioned for a strong growth trajectory, with earnings anticipated to expand by 124.95% annually and revenue projected to increase at 21% per year, outpacing the Chinese market average. Despite recent financial setbacks, including a net loss of CNY 179.23 million in 2024, the company has completed a share buyback worth CNY 71.42 million. However, its forecasted return on equity remains low at 2.8%, and no significant insider trading activity has been reported recently.

- Unlock comprehensive insights into our analysis of Beijing Hotgen Biotech stock in this growth report.

- Our comprehensive valuation report raises the possibility that Beijing Hotgen Biotech is priced higher than what may be justified by its financials.

Jiangsu Nata Opto-electronic Material (SZSE:300346)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jiangsu Nata Opto-electronic Material Co., Ltd. operates in the opto-electronic materials industry and has a market cap of approximately CN¥21 billion.

Operations: The company's revenue is primarily derived from its semiconductor materials segment, totaling CN¥1.60 billion.

Insider Ownership: 18%

Jiangsu Nata Opto-electronic Material is set for substantial revenue growth, forecasted at 21.8% annually—outpacing the Chinese market's 12.9%. While earnings are expected to grow significantly at 24.55% per year, they lag slightly behind the overall market growth rate of 24.6%. The company's return on equity remains modestly low at a projected 14.3%. Recent developments include plans for acquiring a significant equity stake in another company and changes to its bylaws and registered capital structure.

- Get an in-depth perspective on Jiangsu Nata Opto-electronic Material's performance by reading our analyst estimates report here.

- Our expertly prepared valuation report Jiangsu Nata Opto-electronic Material implies its share price may be too high.

Taking Advantage

- Investigate our full lineup of 910 Fast Growing Global Companies With High Insider Ownership right here.

- Contemplating Other Strategies? Trump has pledged to "unleash" American oil and gas and these 20 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Jiangsu Nata Opto-electronic Material, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300346

Jiangsu Nata Opto-electronic Material

Jiangsu Nata Opto-electronic Material Co., Ltd.

Flawless balance sheet with moderate growth potential.

Market Insights

Community Narratives