We Think That There Are Some Issues For Shandong Ruifeng Chemical (SZSE:300243) Beyond Its Promising Earnings

The market for Shandong Ruifeng Chemical Co., Ltd.'s (SZSE:300243) stock was strong after it released a healthy earnings report last week. However, we think that shareholders should be cautious as we found some worrying factors underlying the profit.

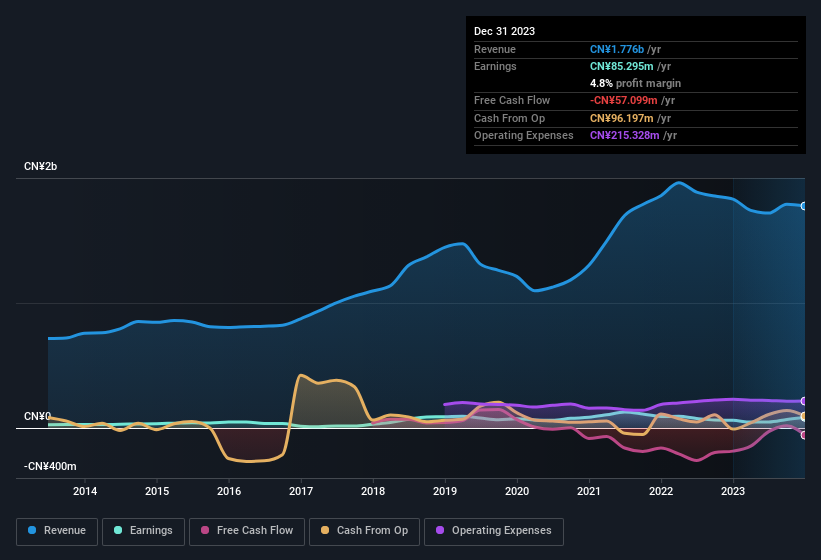

See our latest analysis for Shandong Ruifeng Chemical

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. Shandong Ruifeng Chemical expanded the number of shares on issue by 7.8% over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Shandong Ruifeng Chemical's EPS by clicking here.

A Look At The Impact Of Shandong Ruifeng Chemical's Dilution On Its Earnings Per Share (EPS)

As you can see above, Shandong Ruifeng Chemical's net profit is roughly the same as what it was three years ago. In contrast, its earnings per share is down 2.7% per year over the same period. The profit growth of 40% in the last twelve months certainly seems very impressive. Then again, EPS was only up 38% over that period. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if Shandong Ruifeng Chemical can grow EPS persistently. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Shandong Ruifeng Chemical.

Our Take On Shandong Ruifeng Chemical's Profit Performance

Shandong Ruifeng Chemical shareholders should keep in mind how many new shares it is issuing, because, dilution clearly has the power to severely impact shareholder returns. Because of this, we think that it may be that Shandong Ruifeng Chemical's statutory profits are better than its underlying earnings power. But at least holders can take some solace from the 38% EPS growth in the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into Shandong Ruifeng Chemical, you'd also look into what risks it is currently facing. Case in point: We've spotted 4 warning signs for Shandong Ruifeng Chemical you should be mindful of and 3 of these bad boys make us uncomfortable.

This note has only looked at a single factor that sheds light on the nature of Shandong Ruifeng Chemical's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you're looking to trade Shandong Ruifeng Chemical, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300243

Slight second-rate dividend payer.