Advertisement

3 Global Growth Stocks With High Insider Ownership And 28% Revenue Growth

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by steady interest rates and mixed economic signals, investors are closely watching the performance of various indices. The recent outperformance of value stocks over growth stocks highlights the shifting investor sentiment amid heightened uncertainty and evolving economic forecasts. In such an environment, companies with strong insider ownership and impressive revenue growth can be particularly appealing, as they often signal confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Pharma Mar (BME:PHM) | 11.8% | 40.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 47.2% |

| Vow (OB:VOW) | 13.1% | 111.2% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| CD Projekt (WSE:CDR) | 29.7% | 40.9% |

| Nordic Halibut (OB:NOHAL) | 29.8% | 56.3% |

| Fulin Precision (SZSE:300432) | 13.6% | 78.6% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 60.9% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

We're going to check out a few of the best picks from our screener tool.

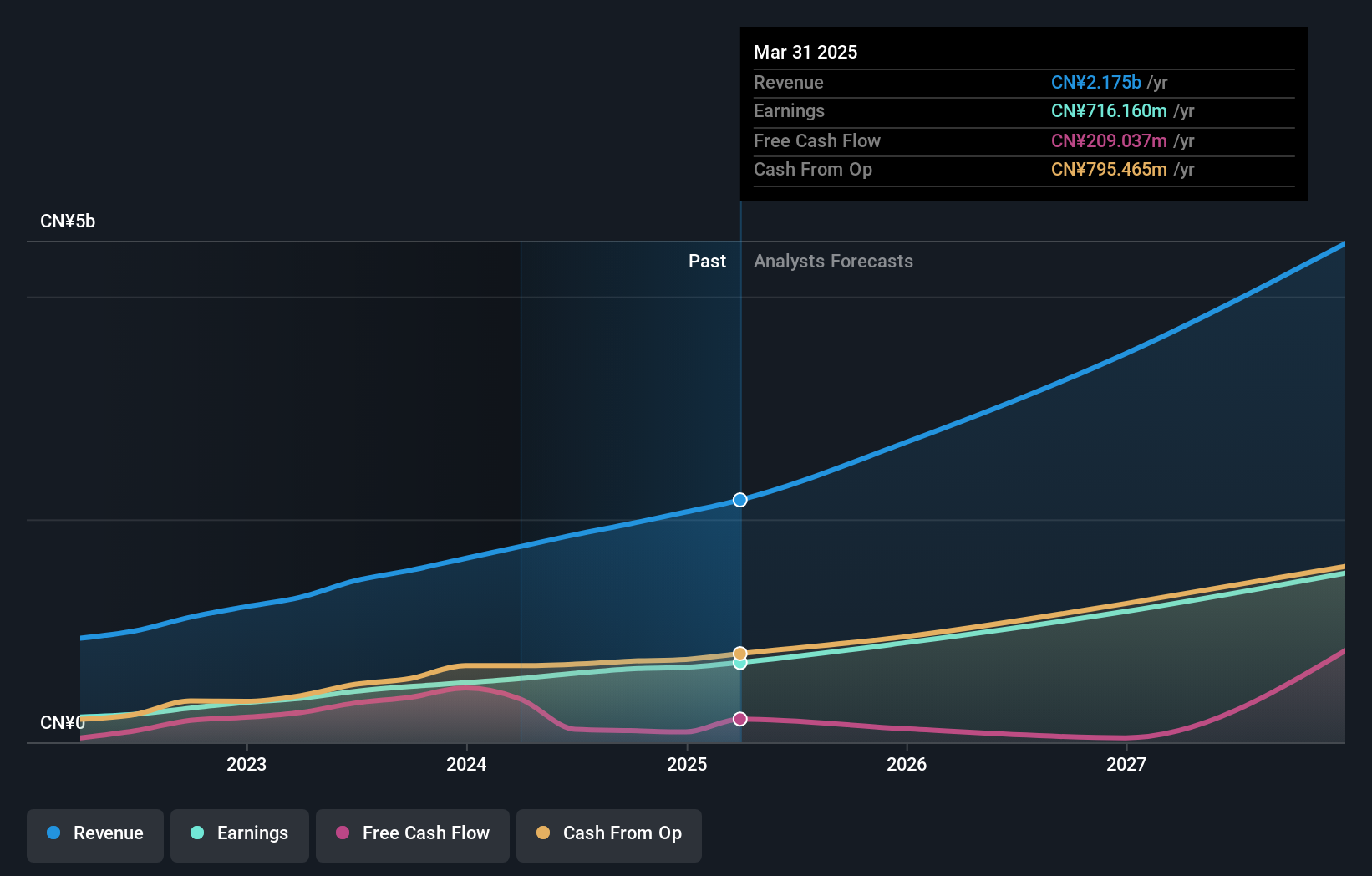

APT Medical (SHSE:688617)

Simply Wall St Growth Rating: ★★★★★★

Overview: APT Medical Inc. focuses on the research, development, manufacturing, and supply of electrophysiology and vascular interventional medical devices in China with a market cap of CN¥36.43 billion.

Operations: The company's revenue from its medical products segment amounts to CN¥2.07 billion.

Insider Ownership: 22.1%

Revenue Growth Forecast: 28.9% p.a.

APT Medical demonstrates strong growth potential with earnings and revenue expected to grow significantly at 29.66% and 28.9% annually, outpacing the broader CN market. Recent financial results show substantial year-on-year growth, with sales reaching CNY 2.07 billion and net income rising to CNY 673.48 million for 2024. Despite no recent insider trading activity, the company's high return on equity forecast of 29.9% supports its position as a promising growth entity with high insider ownership stability.

- Delve into the full analysis future growth report here for a deeper understanding of APT Medical.

- The analysis detailed in our APT Medical valuation report hints at an inflated share price compared to its estimated value.

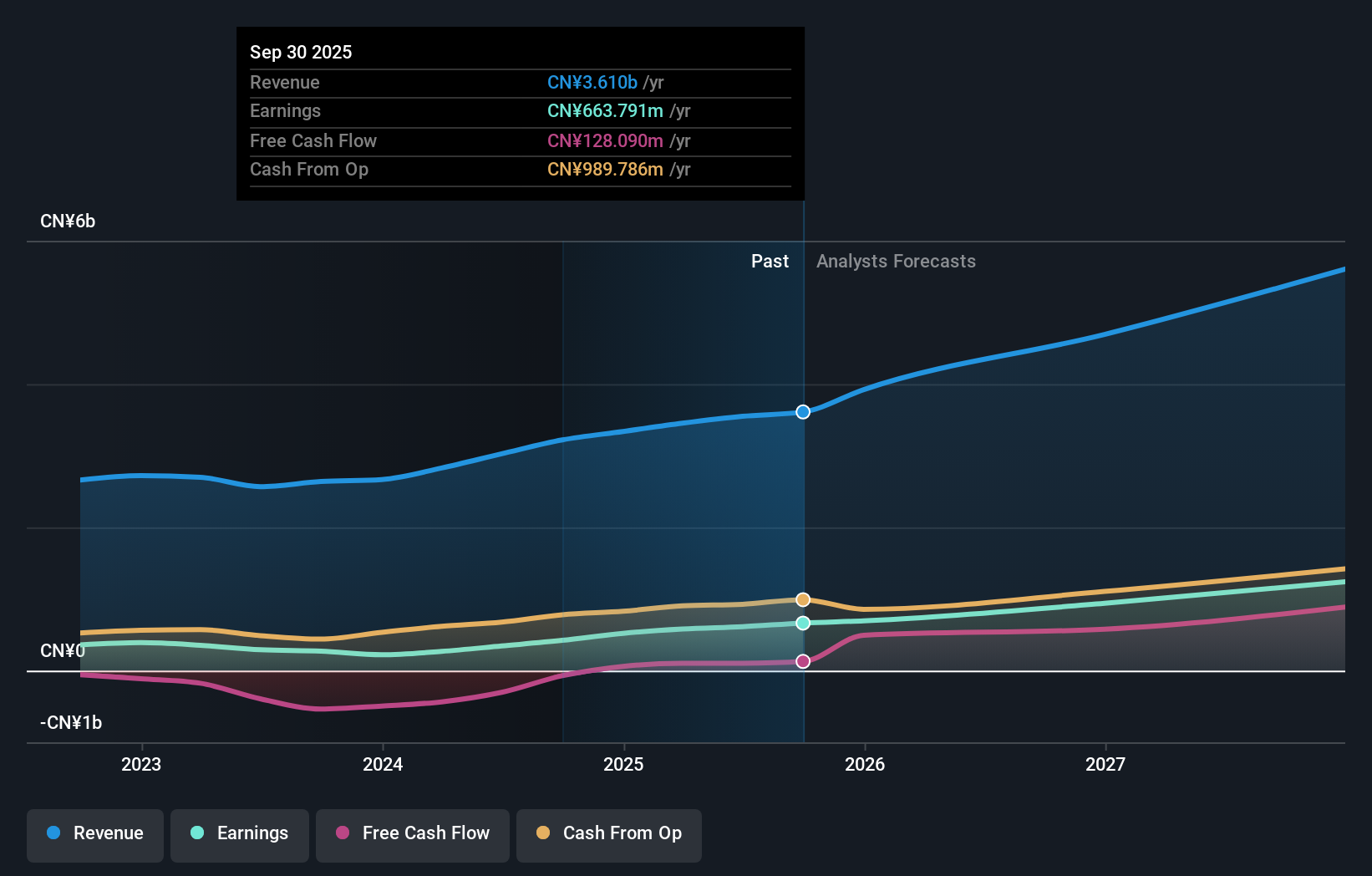

Hubei DinglongLtd (SZSE:300054)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hubei Dinglong CO.,Ltd. operates in the research, development, production, and service sectors for circuit design, semiconductor materials, and printing and copying consumables with a market cap of CN¥26.08 billion.

Operations: The company generates revenue primarily from the Photoelectric Imaging Display and Semiconductor Process Materials Industry, totaling CN¥3.20 billion.

Insider Ownership: 29.9%

Revenue Growth Forecast: 16.7% p.a.

Hubei Dinglong Ltd. exhibits promising growth prospects with forecasted revenue and earnings growth rates of 16.7% and 31.8% annually, respectively, surpassing the broader CN market averages. Despite a lower future return on equity projection of 13.9%, the company's substantial insider ownership aligns with its strong profit trajectory, enhancing investor confidence in its long-term potential. Recent financial updates do not indicate significant insider trading activity over the past three months.

- Take a closer look at Hubei DinglongLtd's potential here in our earnings growth report.

- Upon reviewing our latest valuation report, Hubei DinglongLtd's share price might be too optimistic.

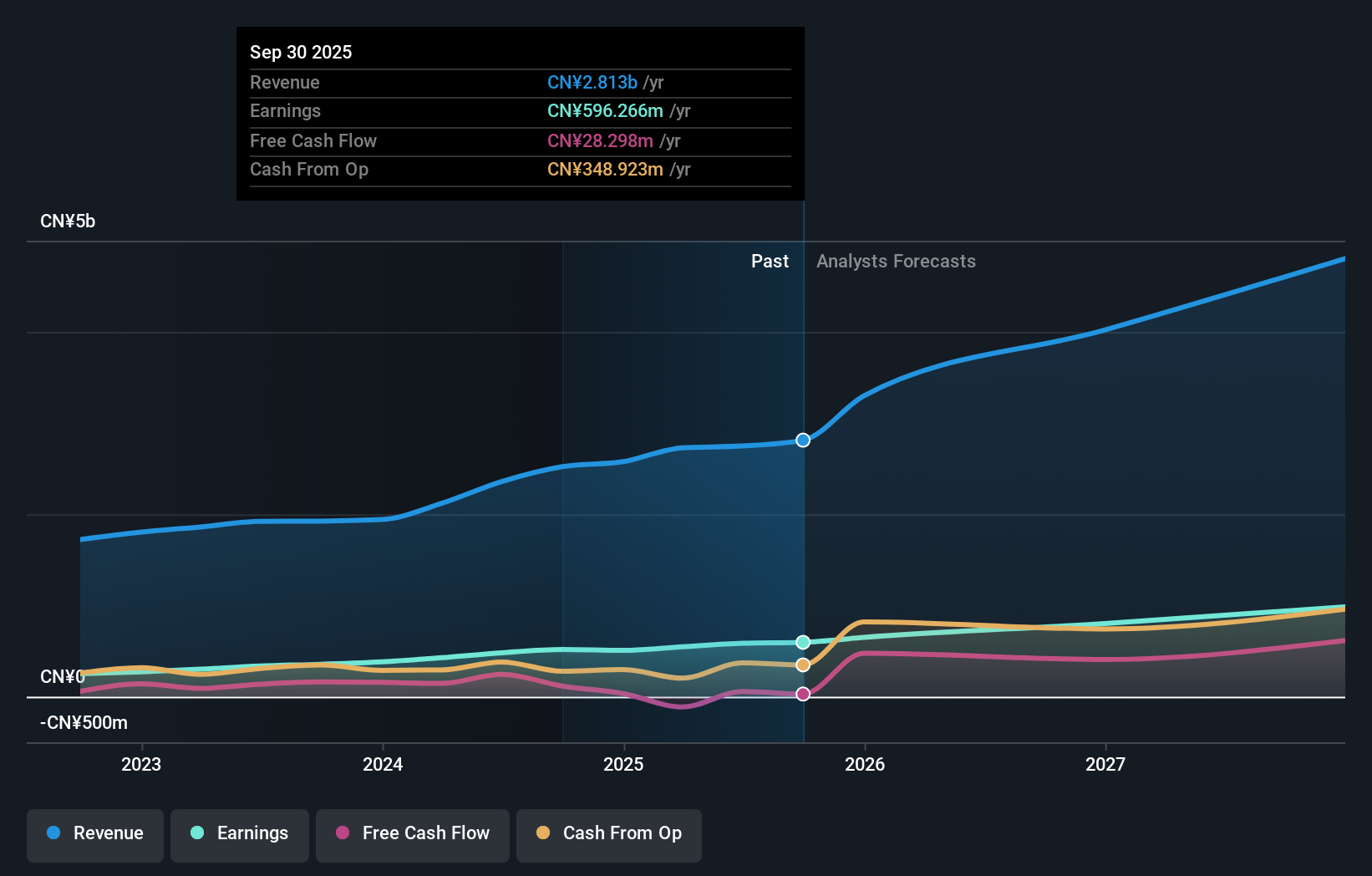

Zhejiang Jolly PharmaceuticalLTD (SZSE:300181)

Simply Wall St Growth Rating: ★★★★★★

Overview: Zhejiang Jolly Pharmaceutical Co., LTD focuses on the research, production, and marketing of Chinese medicinal products both domestically and internationally, with a market cap of CN¥11.23 billion.

Operations: Zhejiang Jolly Pharmaceutical Co., LTD's revenue is derived from its activities in researching, producing, and marketing Chinese medicinal products within China and on an international scale.

Insider Ownership: 23.3%

Revenue Growth Forecast: 22.7% p.a.

Zhejiang Jolly Pharmaceutical's earnings and revenue are projected to grow significantly, outpacing the broader CN market. The company reported a strong increase in sales and net income for 2024, with sales reaching CNY 2.58 billion. Trading at a substantial discount to its estimated fair value, it offers good relative value compared to peers. Despite this growth potential, its dividend is not well covered by free cash flows, and no recent insider trading activity has been noted.

- Click here and access our complete growth analysis report to understand the dynamics of Zhejiang Jolly PharmaceuticalLTD.

- Our expertly prepared valuation report Zhejiang Jolly PharmaceuticalLTD implies its share price may be lower than expected.

Make It Happen

- Dive into all 898 of the Fast Growing Global Companies With High Insider Ownership we have identified here.

- Ready To Venture Into Other Investment Styles? Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Jolly PharmaceuticalLTD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300181

Zhejiang Jolly PharmaceuticalLTD

Engages in the research, production, and marketing of Chinese medicinal products in the People’s Republic of China and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor