Investors Holding Back On Do-Fluoride New Materials Co., Ltd. (SZSE:002407)

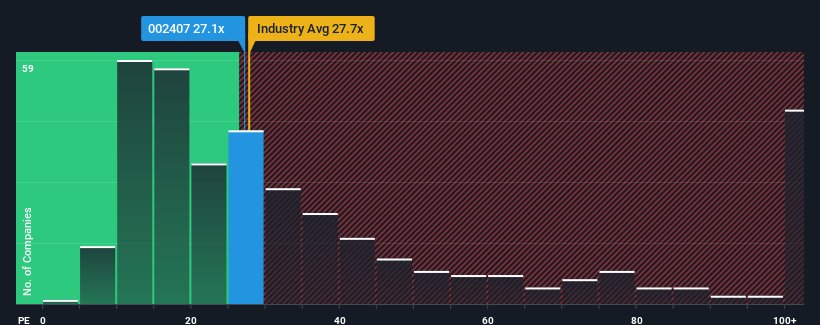

It's not a stretch to say that Do-Fluoride New Materials Co., Ltd.'s (SZSE:002407) price-to-earnings (or "P/E") ratio of 27.1x right now seems quite "middle-of-the-road" compared to the market in China, where the median P/E ratio is around 28x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Do-Fluoride New Materials hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

See our latest analysis for Do-Fluoride New Materials

How Is Do-Fluoride New Materials' Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like Do-Fluoride New Materials' to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 67%. Even so, admirably EPS has lifted 162% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Looking ahead now, EPS is anticipated to climb by 43% per annum during the coming three years according to the three analysts following the company. That's shaping up to be materially higher than the 24% each year growth forecast for the broader market.

In light of this, it's curious that Do-Fluoride New Materials' P/E sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Final Word

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Do-Fluoride New Materials currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

Before you take the next step, you should know about the 3 warning signs for Do-Fluoride New Materials that we have uncovered.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002407

Do-Fluoride New Materials

Engages in the development, production, and sale of inorganic fluorides, electronic chemicals, lithium-ion batteries, and related materials in China and internationally.

High growth potential with adequate balance sheet.

Market Insights

Community Narratives