Advertisement

- China

- /

- Metals and Mining

- /

- SZSE:002203

It's A Story Of Risk Vs Reward With Zhe Jiang Hai Liang Co., Ltd (SZSE:002203)

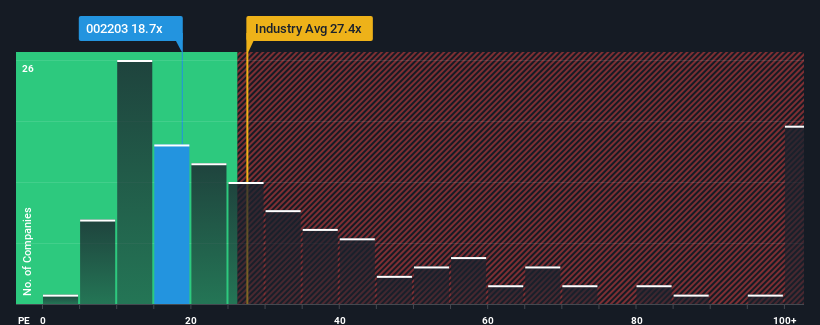

When close to half the companies in China have price-to-earnings ratios (or "P/E's") above 36x, you may consider Zhe Jiang Hai Liang Co., Ltd (SZSE:002203) as an attractive investment with its 18.7x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times haven't been advantageous for Zhe Jiang Hai Liang as its earnings have been falling quicker than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

Check out our latest analysis for Zhe Jiang Hai Liang

How Is Zhe Jiang Hai Liang's Growth Trending?

In order to justify its P/E ratio, Zhe Jiang Hai Liang would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 19% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 3.0% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 45% as estimated by the three analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 40%, which is noticeably less attractive.

With this information, we find it odd that Zhe Jiang Hai Liang is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Zhe Jiang Hai Liang currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

Plus, you should also learn about these 3 warning signs we've spotted with Zhe Jiang Hai Liang (including 1 which is concerning).

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Zhe Jiang Hai Liang might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002203

Zhe Jiang Hai Liang

Engages in the production, sale, and service of copper products, materials of conductors, and aluminum-based materials.

Moderate growth potential second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor