Advertisement

Luyang Energy-Saving Materials Co., Ltd. Just Missed Earnings And Its Revenue Numbers Were Weaker Than Expected

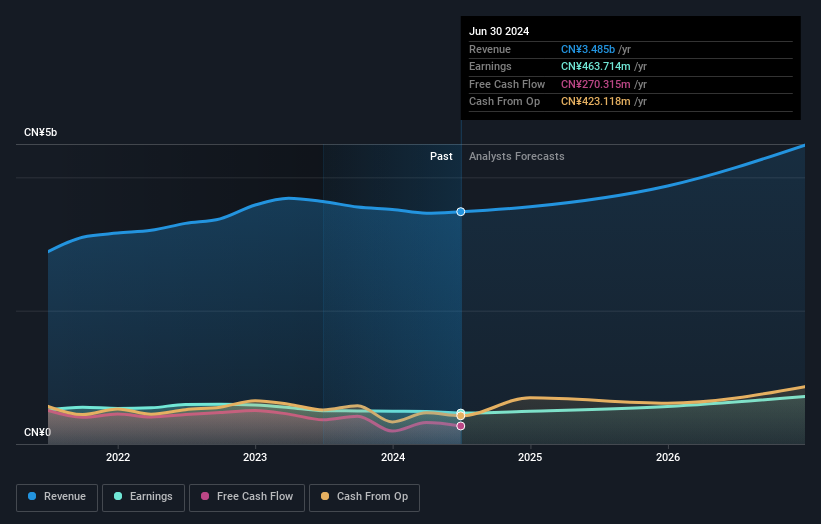

Luyang Energy-Saving Materials Co., Ltd. (SZSE:002088) shareholders are probably feeling a little disappointed, since its shares fell 4.9% to CN¥10.16 in the week after its latest quarterly results. Revenues came in 7.4% below expectations, at CN¥701m. Statutory earnings per share were relatively better off, with a per-share profit of CN¥0.97 being roughly in line with analyst estimates. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for Luyang Energy-Saving Materials

After the latest results, the dual analysts covering Luyang Energy-Saving Materials are now predicting revenues of CN¥3.56b in 2024. If met, this would reflect a modest 2.1% improvement in revenue compared to the last 12 months. Per-share earnings are expected to increase 6.0% to CN¥0.96. In the lead-up to this report, the analysts had been modelling revenues of CN¥3.87b and earnings per share (EPS) of CN¥1.12 in 2024. From this we can that sentiment has definitely become more bearish after the latest results, leading to lower revenue forecasts and a real cut to earnings per share estimates.

The consensus price target fell 20% to CN¥13.60, with the weaker earnings outlook clearly leading valuation estimates.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that Luyang Energy-Saving Materials' revenue growth is expected to slow, with the forecast 2.8% annualised growth rate until the end of 2024 being well below the historical 13% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 16% per year. Factoring in the forecast slowdown in growth, it seems obvious that Luyang Energy-Saving Materials is also expected to grow slower than other industry participants.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Luyang Energy-Saving Materials. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Luyang Energy-Saving Materials' future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Luyang Energy-Saving Materials going out as far as 2026, and you can see them free on our platform here.

It is also worth noting that we have found 1 warning sign for Luyang Energy-Saving Materials that you need to take into consideration.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002088

Luyang Energy-Saving Materials

Researches and develops, produces, and sells energy-saving products in the field of ceramic fiber, alumina fiber, soluble fiber, basalt fiber, and insulating firebrick in China and internationally.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor