- China

- /

- Paper and Forestry Products

- /

- SZSE:002078

Is Shandong Sunpaper (SZSE:002078) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Shandong Sunpaper Co., Ltd. (SZSE:002078) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Shandong Sunpaper

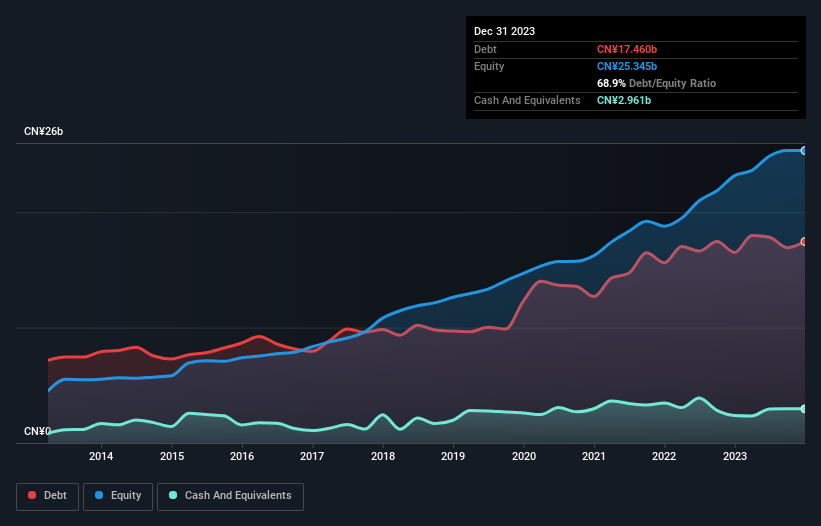

What Is Shandong Sunpaper's Net Debt?

The image below, which you can click on for greater detail, shows that at September 2023 Shandong Sunpaper had debt of CN¥17.5b, up from CN¥16.5b in one year. However, because it has a cash reserve of CN¥2.96b, its net debt is less, at about CN¥14.5b.

How Healthy Is Shandong Sunpaper's Balance Sheet?

According to the last reported balance sheet, Shandong Sunpaper had liabilities of CN¥18.7b due within 12 months, and liabilities of CN¥7.10b due beyond 12 months. On the other hand, it had cash of CN¥2.96b and CN¥5.38b worth of receivables due within a year. So it has liabilities totalling CN¥17.4b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Shandong Sunpaper is worth CN¥38.2b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Shandong Sunpaper has a debt to EBITDA ratio of 2.7 and its EBIT covered its interest expense 4.8 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Unfortunately, Shandong Sunpaper's EBIT flopped 15% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Shandong Sunpaper's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Considering the last three years, Shandong Sunpaper actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

We'd go so far as to say Shandong Sunpaper's conversion of EBIT to free cash flow was disappointing. Having said that, its ability to cover its interest expense with its EBIT isn't such a worry. We're quite clear that we consider Shandong Sunpaper to be really rather risky, as a result of its balance sheet health. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 1 warning sign for Shandong Sunpaper that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002078

Shandong Sunpaper

Produces and sells paper products in China and internationally.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives