Advertisement

- China

- /

- Metals and Mining

- /

- SHSE:600988

Market Participants Recognise Chifeng Jilong Gold Mining Co.,Ltd.'s (SHSE:600988) Earnings Pushing Shares 30% Higher

Chifeng Jilong Gold Mining Co.,Ltd. (SHSE:600988) shareholders would be excited to see that the share price has had a great month, posting a 30% gain and recovering from prior weakness. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 4.0% in the last twelve months.

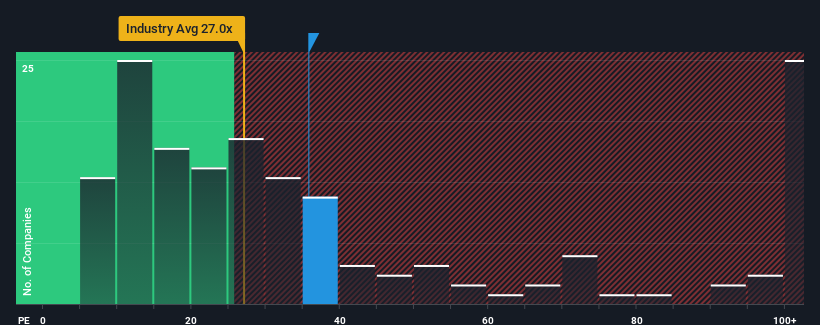

Following the firm bounce in price, Chifeng Jilong Gold MiningLtd's price-to-earnings (or "P/E") ratio of 35.8x might make it look like a sell right now compared to the market in China, where around half of the companies have P/E ratios below 30x and even P/E's below 18x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Recent times have been advantageous for Chifeng Jilong Gold MiningLtd as its earnings have been rising faster than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Chifeng Jilong Gold MiningLtd

What Are Growth Metrics Telling Us About The High P/E?

Chifeng Jilong Gold MiningLtd's P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 81%. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Shifting to the future, estimates from the ten analysts covering the company suggest earnings should grow by 41% each year over the next three years. Meanwhile, the rest of the market is forecast to only expand by 20% per annum, which is noticeably less attractive.

In light of this, it's understandable that Chifeng Jilong Gold MiningLtd's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Chifeng Jilong Gold MiningLtd's P/E

Chifeng Jilong Gold MiningLtd's P/E is getting right up there since its shares have risen strongly. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Chifeng Jilong Gold MiningLtd's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for Chifeng Jilong Gold MiningLtd with six simple checks will allow you to discover any risks that could be an issue.

If you're unsure about the strength of Chifeng Jilong Gold MiningLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600988

Chifeng Jilong Gold MiningLtd

Operates as a gold and non-ferrous metal mining company.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor