- China

- /

- Metals and Mining

- /

- SHSE:600282

Nanjing Iron & Steel Co., Ltd.'s (SHSE:600282) Stock Financial Prospects Look Bleak: Should Shareholders Be Prepared For A Share Price Correction?

Most readers would already know that Nanjing Iron & Steel's (SHSE:600282) stock increased by 5.9% over the past three months. However, its weak financial performance indicators makes us a bit doubtful if that trend could continue. In this article, we decided to focus on Nanjing Iron & Steel's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

Check out our latest analysis for Nanjing Iron & Steel

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Nanjing Iron & Steel is:

8.0% = CN¥2.2b ÷ CN¥28b (Based on the trailing twelve months to September 2024).

The 'return' is the yearly profit. One way to conceptualize this is that for each CN¥1 of shareholders' capital it has, the company made CN¥0.08 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Nanjing Iron & Steel's Earnings Growth And 8.0% ROE

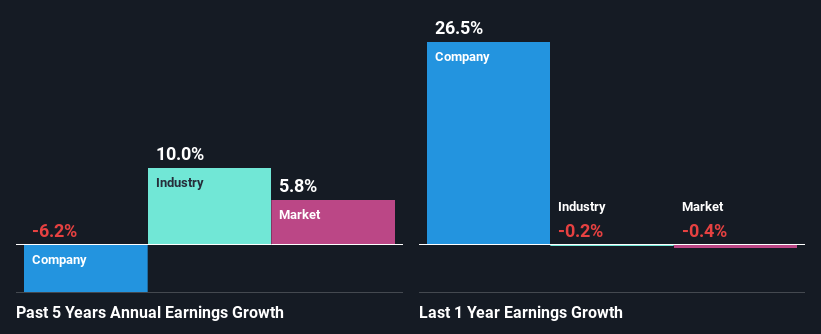

When you first look at it, Nanjing Iron & Steel's ROE doesn't look that attractive. Yet, a closer study shows that the company's ROE is similar to the industry average of 7.4%. But then again, Nanjing Iron & Steel's five year net income shrunk at a rate of 6.2%. Bear in mind, the company does have a slightly low ROE. Therefore, the decline in earnings could also be the result of this.

So, as a next step, we compared Nanjing Iron & Steel's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 10% over the last few years.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is Nanjing Iron & Steel fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Nanjing Iron & Steel Efficiently Re-investing Its Profits?

Nanjing Iron & Steel's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 71% (or a retention ratio of 29%). With only very little left to reinvest into the business, growth in earnings is far from likely. You can see the 2 risks we have identified for Nanjing Iron & Steel by visiting our risks dashboard for free on our platform here.

Additionally, Nanjing Iron & Steel has paid dividends over a period of seven years, which means that the company's management is rather focused on keeping up its dividend payments, regardless of the shrinking earnings.

Summary

On the whole, Nanjing Iron & Steel's performance is quite a big let-down. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

Valuation is complex, but we're here to simplify it.

Discover if Nanjing Iron & Steel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600282

Nanjing Iron & Steel

Produces and sells steel and related products in China.

Proven track record and fair value.